Sigachi Industries Ltd.

This is the market for you the stock is down -55% from its Day -1 listing price but still 60% up from its IPO price, and the stock listed at a 252% premium over the issue price of ₹163 apiece but has the recent correction made it a value buy? let’s try to analyze it in this post.

What does this company do?

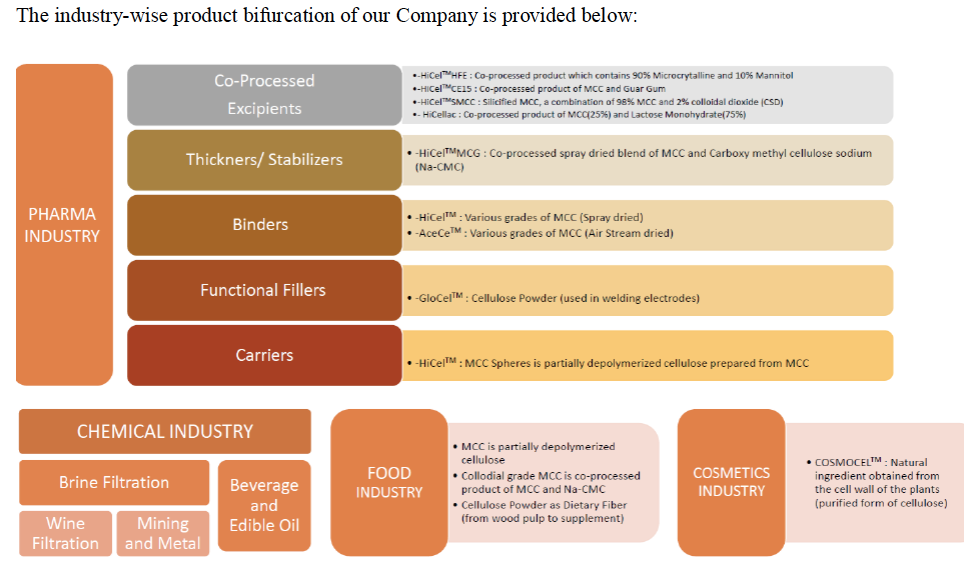

The company is in the business of manufacturing Microcrystalline (MCC)

Microcrystalline is refined wood pulp and chemically inert substance, extensively used in food, pharmaceuticals, cosmetic, and polymer composite industries. This is owing to its non-toxicity, renewability, biodegradability, and mechanical properties such as high surface area and biocompatibility. In processed food products, it is used as an emulsifier, stabilizer, anti-caking agent, texture modifier, stabilizer, fat substitute, and suspending agent.

Furthermore, MCC (Microcrystalline Cellulose) is widely used in pharmaceuticals, owing to its tasteless, odorless, and chemical inertness properties.

The good thing about this product is it enjoys the low input cost moat as I explained in my portfolio update earlier (snapshot below).

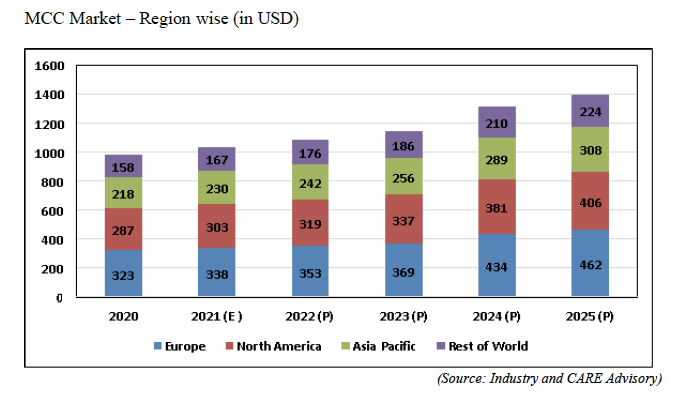

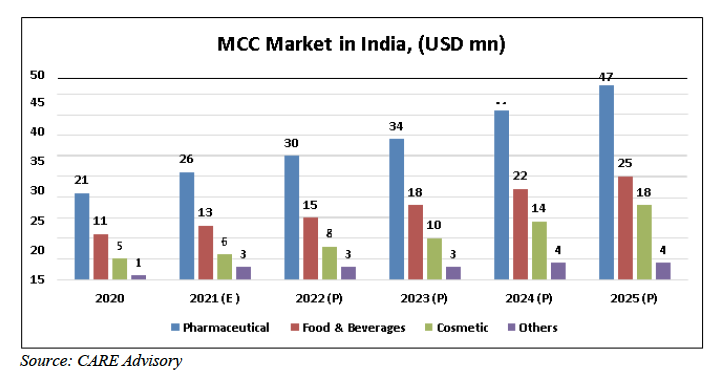

The problem with low input cost businesses is their market size also remains relatively small - “Microcrystalline Cellulose Market size is forecast to reach USD 1.4 billion by CY 2025, growing at a CAGR of 7.25% during CY 2020-2025.”

Whereas the size of the end industry it serves- the global pharmaceuticals market is expected to be USD 1228.45 Billion.

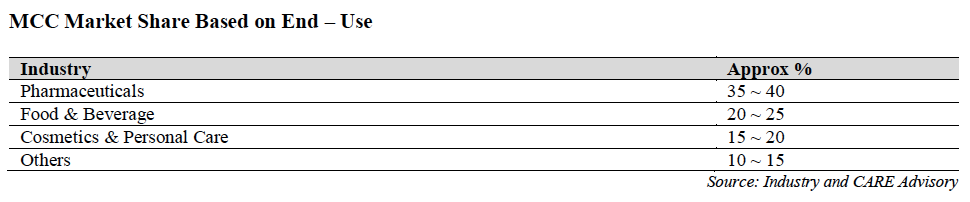

On the basis of application, the MCC market has been classified into food & beverage, pharmaceutical, cosmetics & personal care, and others. Pharmaceutical was the largest application of MCC in CY 2020, in terms of value and volume. MCC is a vital component that is used in every form of oral dosage, which includes pellets, capsules, tablets and sachets. It is increasingly being used in quick-release tablets & liquid dosage forms, sustained-release multiparticulates & matrix tablets dosage forms, topical formulations, and chewable & effervescent tablets.

Moreover, increasing demand for low fat food, owing to growing obese population in the region is a factor expected to support growth of the market over the forecast period. This is as MCC is gaining popularity as a cellulose-based fat replacer and is widely used in sauces, dairy products, salad dressings, and frozen desserts.

Asia Pacific is projected to be the fastest growing region in the global microcrystalline cellulose market, registering the highest CAGR of 7.19% over CY 2020-2025 (the forecast period).

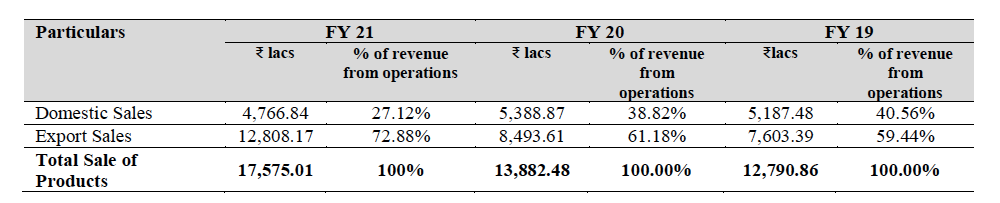

In India where Sigachi is market leader the market size is about 35 million US (Rs 280 Cr.) Sigachi yearly TTM sales today is Rs 267 Cr of which 75% of revenue comes from export.

Obviously, the question is of this Rs 280 Cr market size in India why the company has only been able to capture just about Rs 70 Cr?

One reason could be company makes better margins while exporting their products and they were running at 90+ capacity pre-IPO. Maybe the goal is to add more capacity and try gaining market share in India but their competitor also enjoys the same “low input cost to their customer” moat.

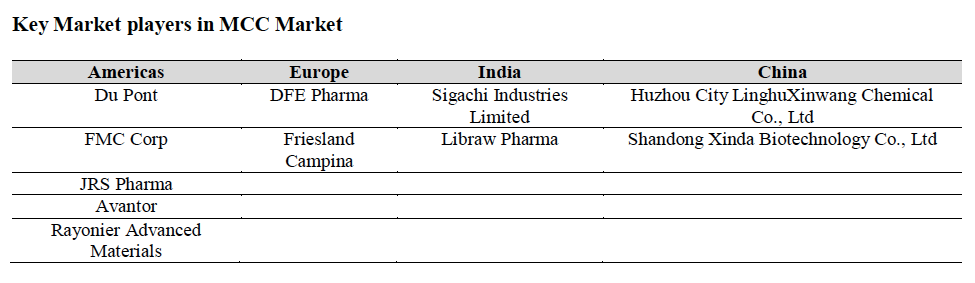

Key competitors in the market -

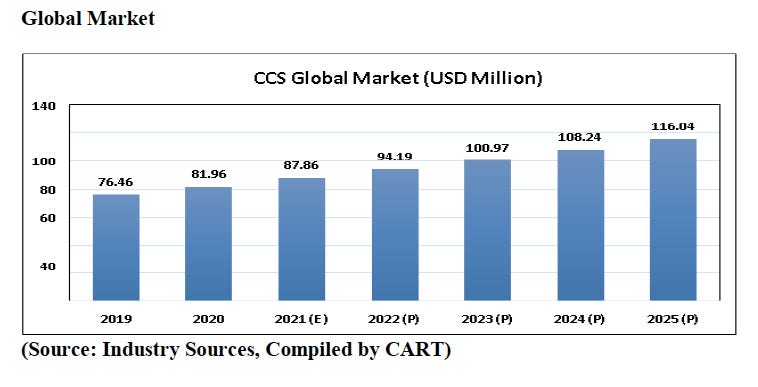

The company also from the IPO processed planning to venture into manufacturing Croscarmellose Sodium Industry (CCS)

CCS is a grayish-white or white powder and has no odor. It is used as a disintegrant in the pharmaceutical formulation and provides long-term stability & also used in the formulation of pharmaceutical tablets, pellets, and capsules which are manufactured by dry granulation, wet granulation, or by direct compression.

It has an even smaller just Rs 80’ish million USD market size today.

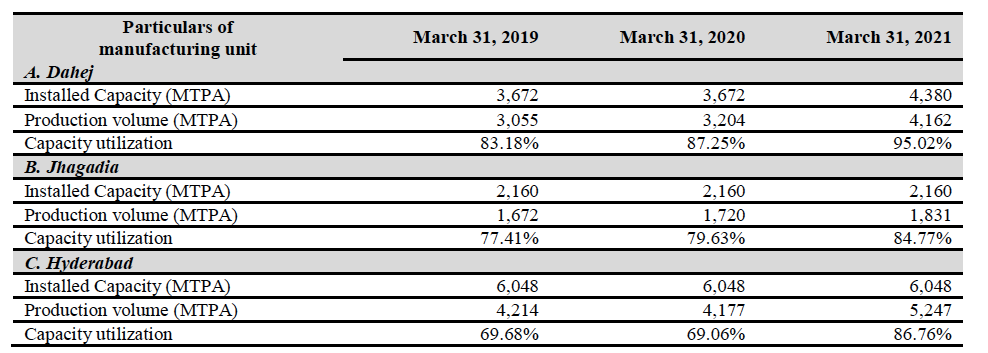

Presently, the company manufactures 59 different grades of MCC at their manufacturing units, situated in Hyderabad and Gujarat with an aggregate installed capacity of 11,880 MTPY.

They have also entered into operations and management agreements with Gujarat Alkalies and Chemicals Limited (“GACL”) for operating and managing the manufacturing units owned by GACL and for contract manufacturing of sodium chlorate, stable bleaching powder, and poly aluminum chloride in the said units.

Innovation -

In the year 2011, our Company was awarded the first prize at the Innovation Award Ceremony for MSME 2011 for presenting a model on the filtration process of wet MCC cakes, which reduces the time taken for filtration and provides an optimum pH level for such cakes, for further processing.

Since incorporation, it has been our Company’s vision and focuses to manufacture and supply premium quality products to our customers, which has enabled them to expand their business operations globally and receive certifications from renowned international bodies for our good manufacturing practices and efficient process techniques.

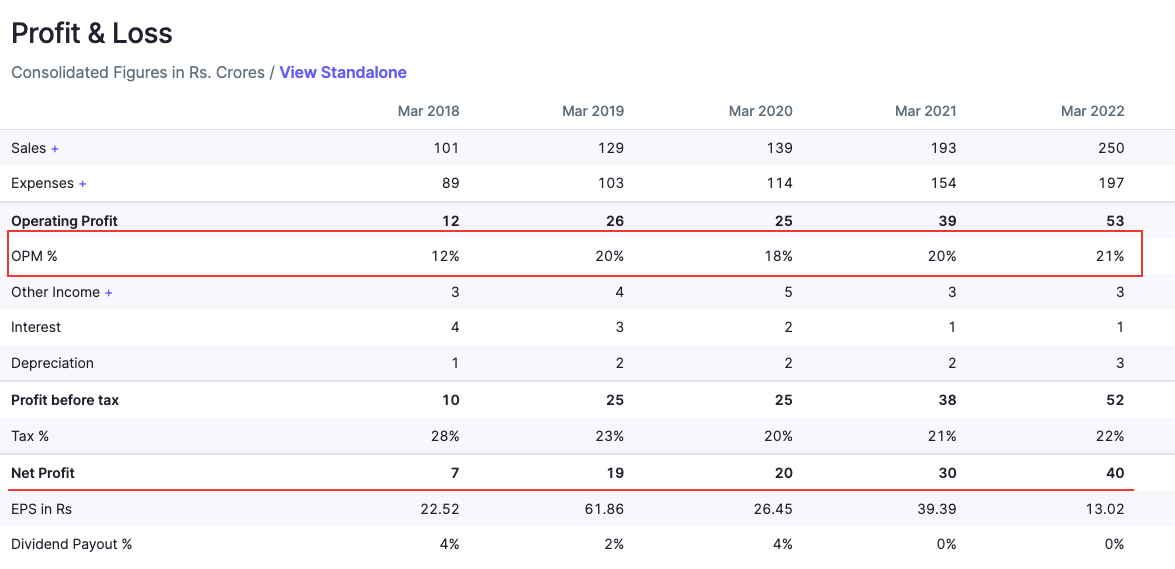

As shown in the above pic the key reason they were able to clock 25% cagr kind of growth pre-IPO years is due to their more focus on growing export revenue which lead to an increase in OPM. Which kind of explain why despite being the market leader in the Rs 280Cr size of the domestic market today they sell only about Rs 70 worth of MCC (export margins are better Vs domestic).

Management Team -

Founding members are

Promoters - Rabindra Prasad Sinha

Whole-time Directors - Chidambarnathan Shanmuganathan.

They are still actively involved in the strategic decision-making for the Company.

Rabindra Prasad Sinha played an instrumental role in setting up our wholly owned subsidiary, Sigachi US Inc., and in the expansion of export operations.

Chidambarnathan Shanmuganathan has an experience of more than five decades in the field of a variety of chemicals and derivatives of cellulose. He has played an instrumental role in expanding the domestic operation of the Company and in setting up manufacturing units in Gujarat.

He also helped Company diversify the operations to include operation and maintenance of chemical manufacturing units for a public sector undertaking such as Gujarat Alkalies and Chemicals Limited.

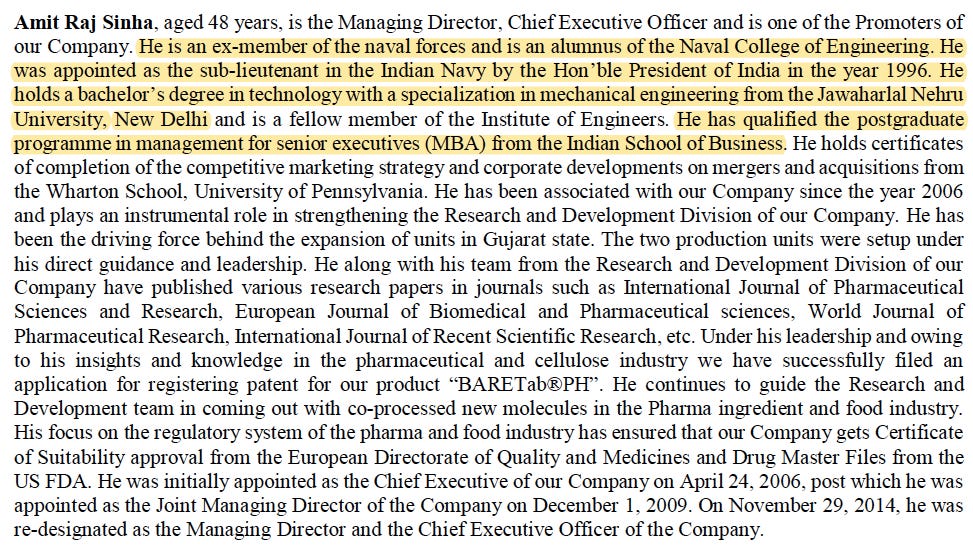

Promoter, Managing Director and Chief Executive Officer, Amit Raj Sinha has been instrumental in strengthening the R&D Division of our Company.

He along with his team from the R&D Division of the Company has published various research papers in renowned journals such as the International Journal of Pharmaceutical Sciences and Research, European Journal of Biomedical and Pharmaceutical Sciences, World Journal of Pharmaceutical Research, and International Journal of Recent Scientific Research, etc. Under his leadership and owing to his insights and knowledge in the pharmaceutical and cellulose industry we have successfully filed an application for registering our patent titled as “BARETabPH”.

More about the guy who is running the show -

The objective of the IPO -

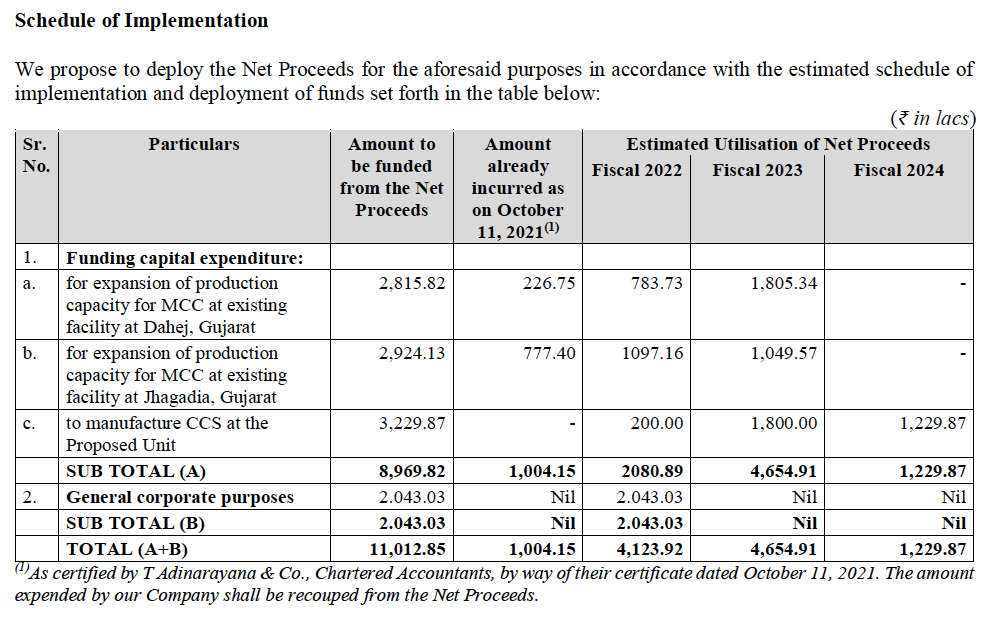

Raised Rs 110 Cr, To deploy on the following -

1. Funding capital expenditure:

for expansion of production capacity for microcrystalline cellulose (“MCC”) at Dahej, Gujarat;

for expansion of production capacity for microcrystalline cellulose (“MCC”) at Jhagadia, Gujarat; and

to manufacture Croscarmellose Sodium (“CCS”), modified cellulose used as an excipient at Kurnool, Andhra Pradesh.

2. General Corporate Purposes.

80-90% of the Capex will be done by FY23 and by FY24 all Capex is planned to be finished.

How much capacity addition is planned in Total? ( and at full capacity how much Revenue can be increased)

Capacity pre-IPO -

The plan is to increase the -

Dahej Capacity by 76%.

Jhagadia Capacity by 150%

For CSS - The Proposed Unit is expected to have a capacity of 4 MT per day for CCS.

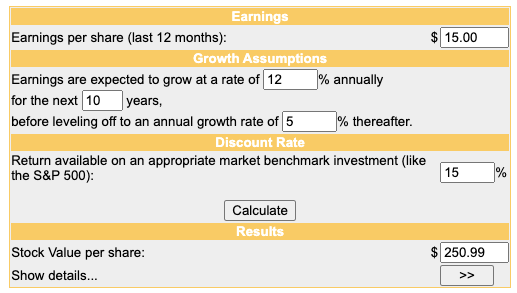

If we assume they will be able to achieve 90% of overall newly added capacity utilization by 2030, i.e their revenue will grow by 10% cagr + inflation 5% cagr (+15% cagr) from 2023 onwards.

Today markets are conservatively pricing in 12% cagr kind of growth for 10 years and 5% terminal growth with a 15% discount rate. (which I think is a reasonable assumption by the market, certainly not a pipe dream growth scenario for this company to achieve)

Key Focus Areas - (From DRHP)

Our strategic objective is to improve and consolidate our position as one of the leading excipient manufacturers in India with a continuous growth philosophy and to enter value services.

achieve maximum operational efficiency.

strengthen and expand our market position and product portfolio.

enhance our depth of experience, knowledge-base, and know-how and

increase our network of distributors, customers, and geographical reach.

MANUFACTURING PROCESS

Key Raw Material Procurement -

The major raw material used during the manufacture of MCC is purified dissolving wood pulp bales. These are imported from Canada, South Africa, Thailand, Indonesia, and America from various suppliers. The chemical and physical properties of the pulp determine the final quality of our finished products. The wood pulp bales are imported based on the quality and the price at which they are available from the suppliers.

If you watch some youtube videos on this company by influencers - they have mentioned this as an anti-thesis pointer stating wood pulp comes from trees and for Environmental reasons they may not be allowed to cut the trees.

Whereas it looks like a global commodity that can be sourced from various countries (all countries can’t have Greta Thunberg protecting tress at the same time if that happens we will not have many medicines for treatments in the market) and the company has 100% ability to pass on input cost inflation to their customer. Also, because 75% of the revenue comes from exports they are naturally hedged in their currency risk (importing raw materials in dollars then exporting value-added finished goods in dollars).

Capacity Installed and Capacity Utilisation -

Pre IPO they were working at 90% Capacity utilization, the reason why money has been raised to expand capacity (not for the PE investors to exit).

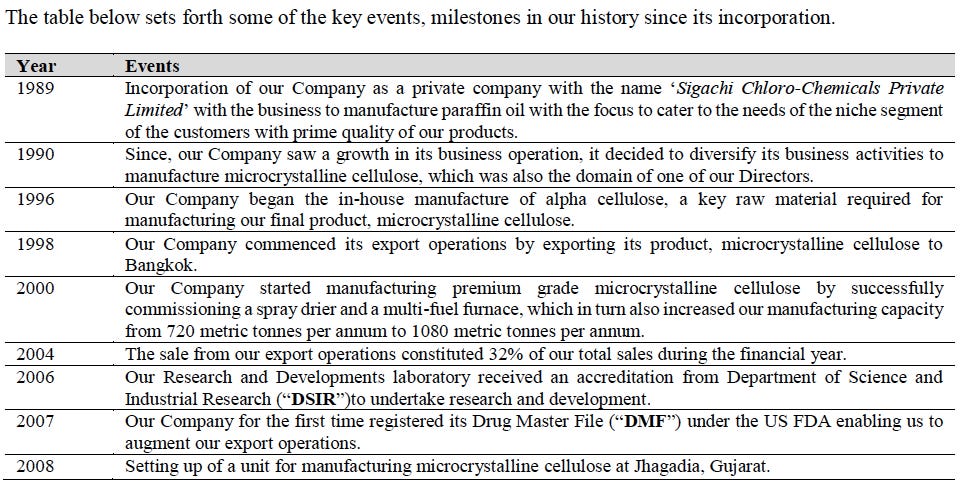

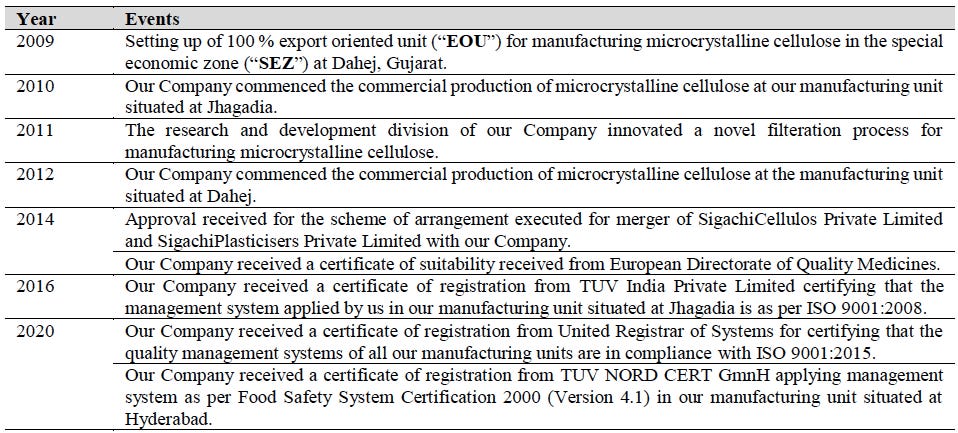

Major Events and Milestones -

Any Red Flags?

Defaults or Rescheduling of Borrowings with Financial Institutions/ Banks?

There are no defaults or rescheduling of borrowings from financial institutions or banks or conversion of loans into equity in relation to our Company.

Revaluation of assets?

The company has neither revalued its assets nor has it issued any Equity Shares (including bonus shares) by capitalizing on any revaluation reserves in the last ten years.

Holding Company?

The company does not have a holding company.

Subsidiaries of our Company?

The company has a wholly owned subsidiary, namely Sigachi U.S., Inc.

Associate or Joint ventures of our Company?

The company does not have any joint ventures or Associate Companies.

Strategic and Financial Partners?

The company does not have any strategic and financial partners.

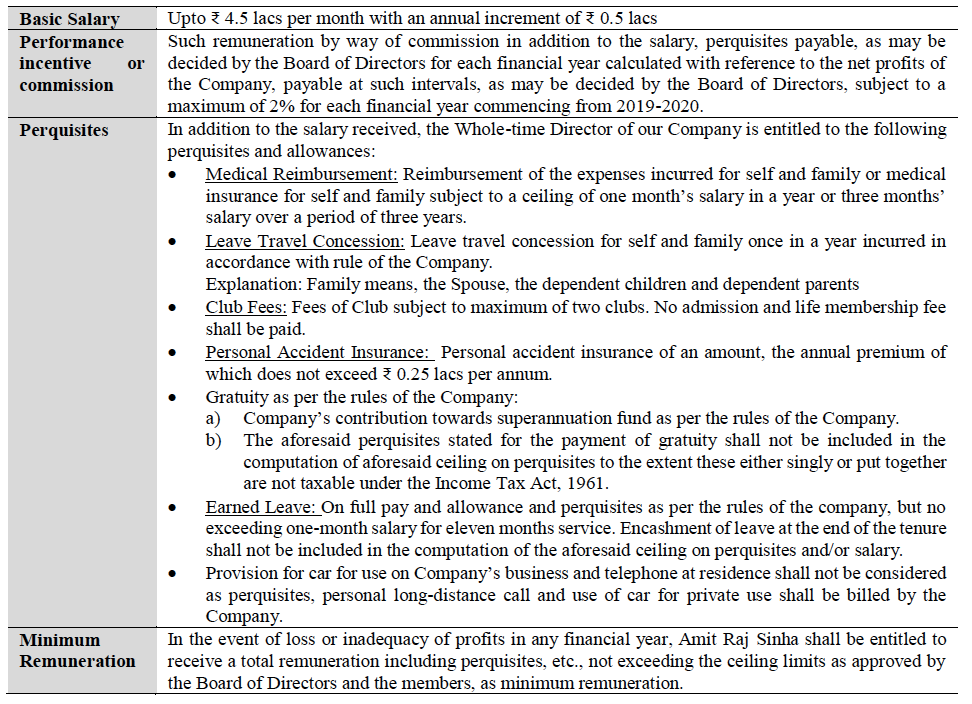

Promoter salary check? (Nothing Alarming)

Amit Raj Sinha -

Similar salary structure for the other two promoters founder Rabindra Prasad Sinha (Father of Raj) & Chidambarnathan Shanmuganathan.

Customer concentration risk? (yes)

These amounts derived from our top five customers, were 53.13%, 47.93%, 38.36%, and 41.49%, respectively.

Sector concentration risk? (yes - pharmaceutical 75% of revenue)

As of June 30, 2021, the revenue from the pharmaceutical, food, nutraceuticals, and cosmetic industries was Rs. 3,785.77 lakhs, Rs. 504.77 lakhs, Rs. 504.77 lakhs, and Rs. 252.38 lakhs respectively, which account for 75%, 10%, 10%, and 5% respectively of our revenues.

Related Party Transactions -

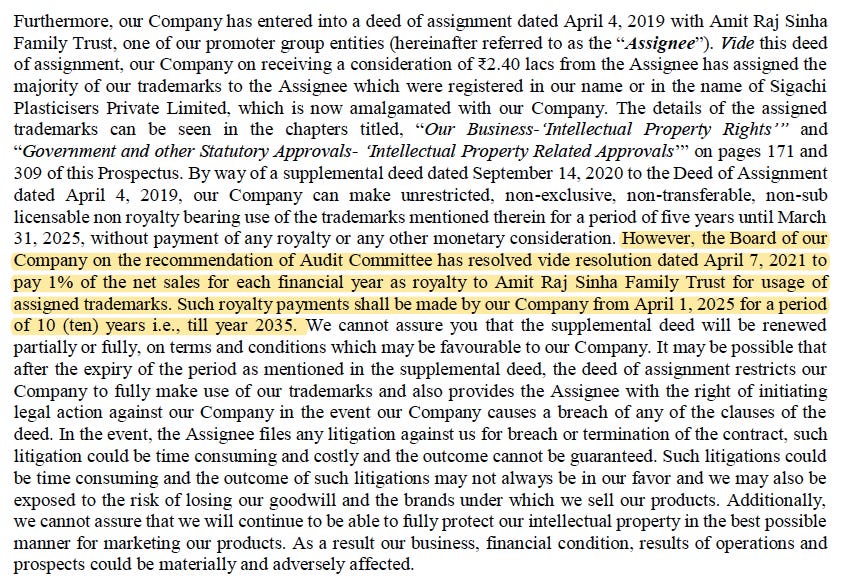

Amit Raj Sinha Family Trust owns certain product trademarks for it Family trust will receive 1% of revenue from 2025 till 2035 as a royalty.

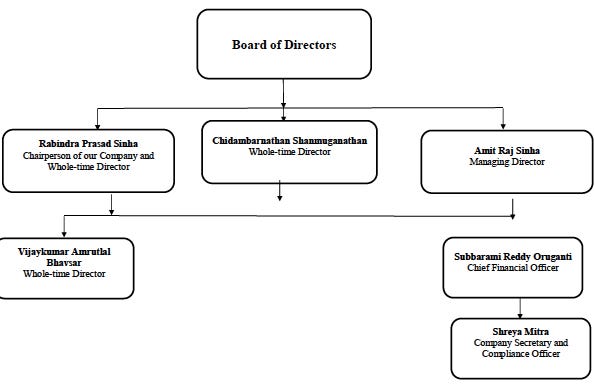

Board Structure -

Snippets from earning call -

The company mainly supplies excipients to the recession-proof pharma industry and has the ability to pass on the input cost inflation.

How can they win market share? because their competitor enjoy similar moat (low input cost for customers)

Interesting answer - when asked why have you been able to grow 25% cagr in last 5 years.

CFO adding to it -

Would love to know your views about the company, Do share your view in the comment section, and don’t forget to share it with friends.

BLOGS ARE NOT A RECOMMENDATION SERVICE – These are my personal views about Business Quality, Management Quality, Business Execution & Performance.

Thanks,

Dhruva Pandey

Email : dhruva.pandey@outlook.com

Twitter : https://twitter.com/Dhruvapandey

Nice writeup Dhruv. But don't you think that even in a business with a distinct competitive advantage they have a key man risk (Mr. Sinha). wouldn't it mean that there future growth rather depends on the ability of the management rather than the industry environment? Also, can it be a case for appreciating luck as skill (Post 2018 it has been a good for pharma companies)?

Also I did some distributor visit for channel check posing as an MCC customer.

Two observations came in: too much commoditization and no brand recall. In fact 6 out of 11 distributors did not even recommend sigachi since cheaper options of same quality were available ( Quality is solely their opinion)