Quarterly Portfolio Update

Quarterly Portfolio Update

What HDFC bank is pricing in today ?

Since the December update, there haven't been many changes in my portfolio. Whatever extra cash I've had, I've mostly invested in buying shares of HDFC and Kotak Bank. The reason is simple: I cannot find any convincing reason not to do so. I don’t see anything structurally changed for the banks. Although some people are saying the biggest structural change now is due to higher financial activity, as people aren’t keeping money in the bank; instead, they are immediately moving it to financial assets rather than making FDs, which the generation of the 60s and 70s used to do. This change in customer behavior is leading to a reduction in NIMs for the banks, and obviously, the impact of this will be higher for retail-focused banks such as HDFC Bank.

Initially, this made me think, "Oh, that's a real danger, as I never keep money idle in a bank account, and if this becomes widespread, that's a structural change." And if the market hasn't priced this in, then I have to revalue the bank. But second-level thinking made me question this thesis again. Let's say person A receives their salary on day 1 and immediately moves it to buy stocks, ETFs, or mutual funds. Then there must be a seller on the other end who is doing the reverse, and ultimately, money is getting transferred from person A's bank account to person B's bank account. Now, it depends on what person B is going to do. They may end up buying some other stock from person C, in which case the money will move into person C's bank account. Or person C might end up buying an IPO, in which case the money will move into the company's bank account, which will further use this IPO raised money to invest in various assets, thereby moving the money into many other bank accounts. I hope the point is clear that ultimately money has only one destination, which is a bank account, unless someone idiot is keeping it in a PayTM wallet or under the mattress. The claim that banks are losing low-cost deposits is false. Yes, there will be some impact of people moving away from FDs to stocks, but that's not the reason for NIMs going down significantly.

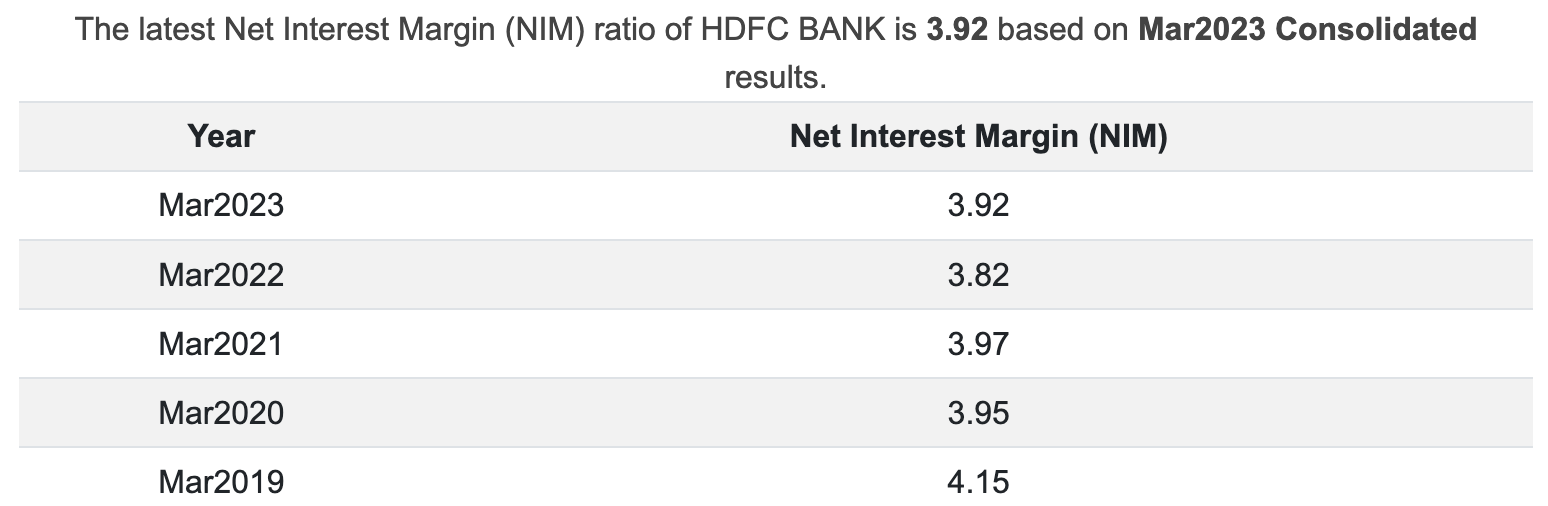

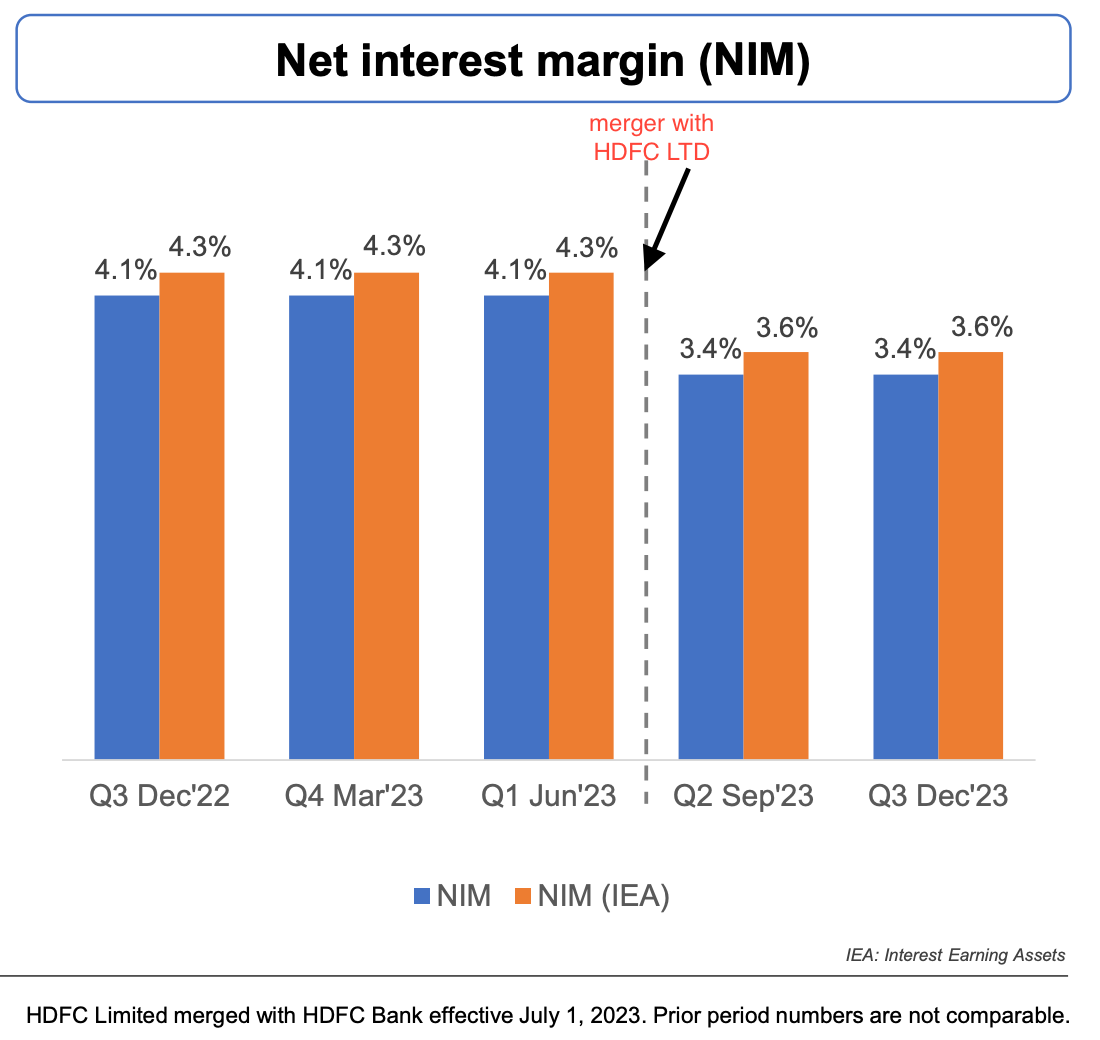

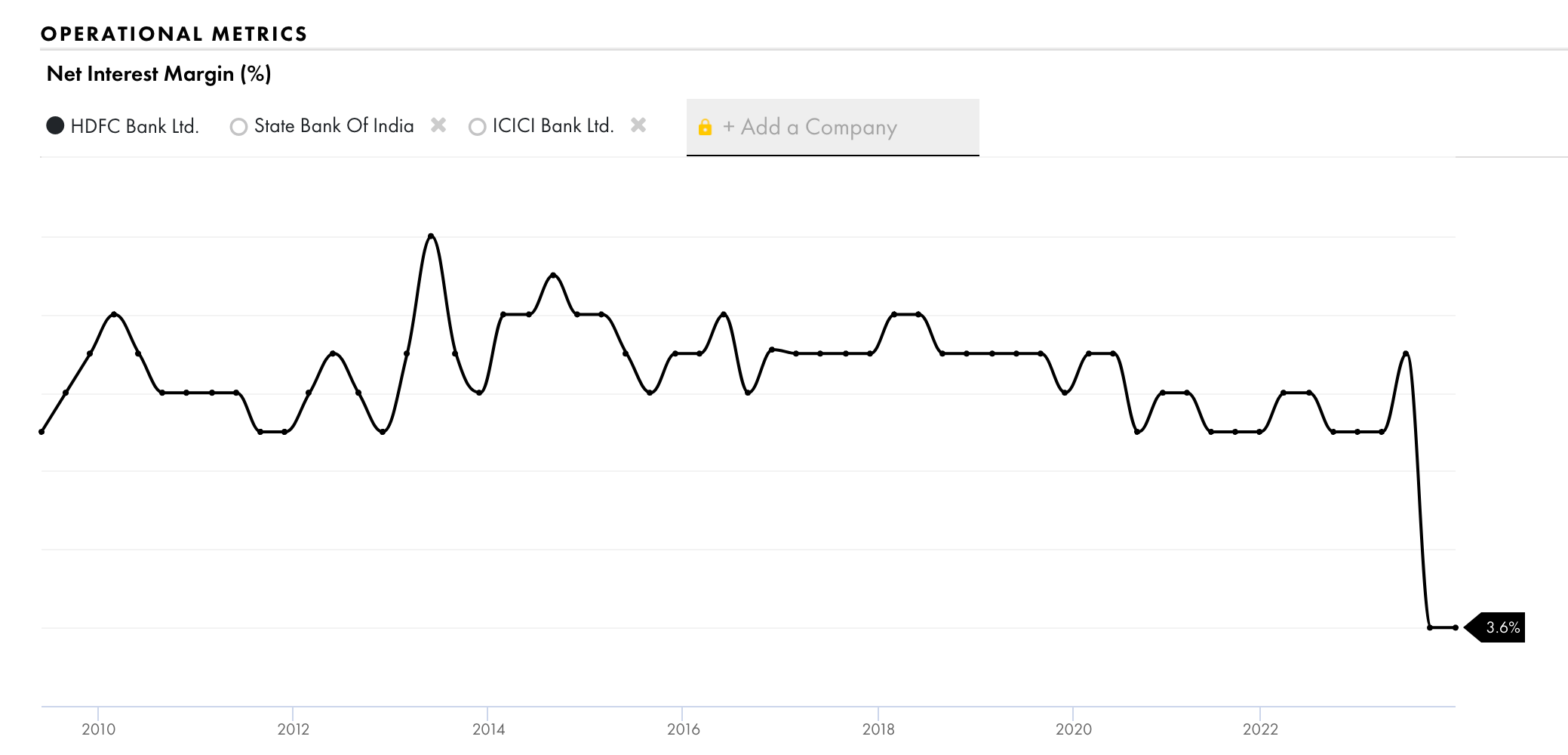

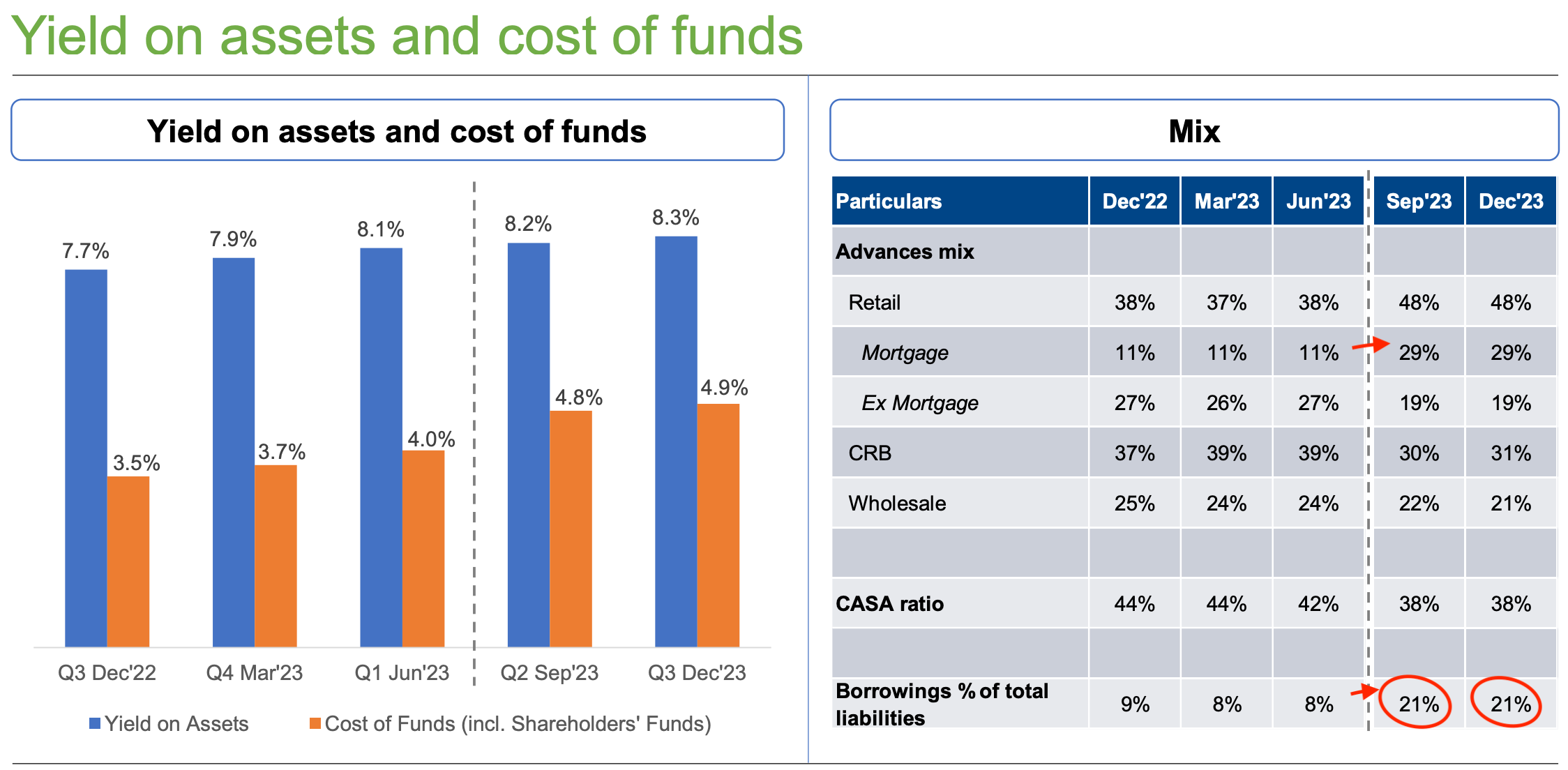

Now lets look into the long term NIMs data of HDFC Bank -

Pre Covid -

Post Covid -

HDFC NIM -

The sudden drop in NIM (Net Interest Margin) made the market nervous, which I suppose is lower than the expectation post-merger. Although management has clarified that by replacing high-interest liabilities of NBFC HDFC Ltd. with low-interest deposits over the next 2-3 years, the NIMs will normalize back to 4%.

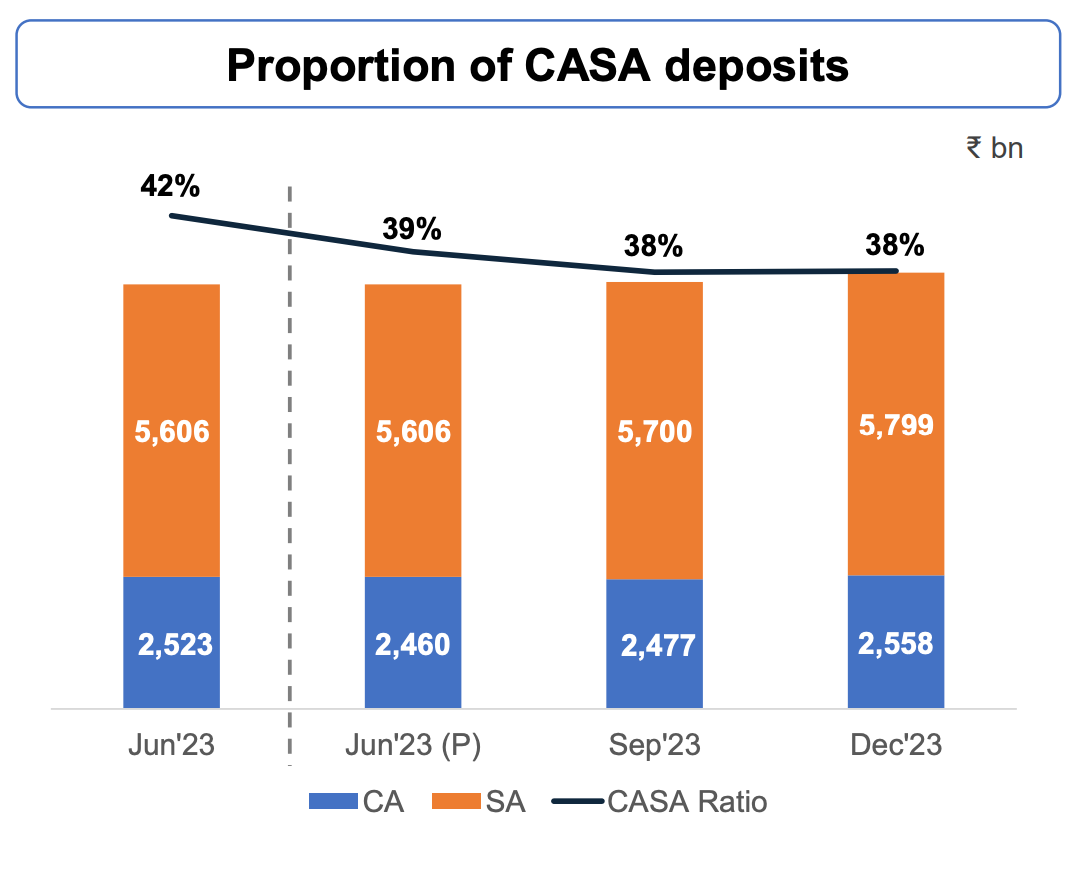

ollowing the merger, there has been a drop in CASA (Current Account Savings Account), which sparked rumors suggesting that people are not keeping funds in their bank accounts and are instead moving their money into financial assets.

Which is clearly reflecting on COF, which have gone up more than Yield on assets post merger.

Regarding the Asset/Liability Mix, it was anticipated that due to the merger, the percentage of Mortgages in total assets would significantly increase from 11% to 29%. The most notable observation is the rise in Borrowing as a percentage of total liabilities, which surged from 8% to 21%, directly contributing to the contraction of NIM.

Does it means the merger gone wrong? or

its no more a great run bank? or

Valuation is justified?

There are obvious benefits of merger

cross-selling of products and expansion of customer base from HDFC

utilising HDFC Bank's low-cost funds from deposits to finance housing loans, thereby improving NIMs.

These two benefits in itself are huge but they will take sometime to bear its fruits but the strategy is simple - Use extensive network of HDFC branches to offer home loan and replace high cost borrowings of HDFC LTD with low cost CASA.

Due to merger from asset side they have pulled in the next 5 to 10 years growth into the present but they have to execute it now from the liability side.

The reason HDFC bank strategy is gathering as much as low cost deposit they can in next 5 years - the only obvious way to do that is by increasing tier-2 / tier-3 / rural penetration.

The growth in deposits at the new branch is not expected to be immediate; typically, it takes 2-3 years for the branches to mature. Therefore, the strategy will test the patience of the markets.

Based on my limited experience in the stock markets, I've observed that the markets tend to disregard events or projections that are three years away. However, if you can accurately predict the impact of a company's expansion three years in advance (which is not factored into market valuations), there is potential to generate significant alpha.

The markets are extremely good at pricing in the next quarter and subsequent one maybe. its extremely hard to have a significant edge over the market by predicting better next quarterly results than the markets. However, there's a notable opportunity to outperform the markets by making long-term bets. Often, markets fail to factor in long-term changes into the valuations.

I don’t have any reason to believe over the next 3 to 5 years management won’t be able to execute on these two strategies -

cross-selling of products and expansion of customer base from HDFC

utilising HDFC Bank's low-cost funds from deposits to finance housing loans, thereby improving NIMs.