MapMyIndia Ltd.

MapMyIndia Ltd.

New Age Tech IPOs Corrected Enough? business model, valuation, intrinsic value.

MapMyIndia offers multiple, digital mapping, navigation, and geospatial tech offerings and currently has a client base of 2,000 enterprise customers. “From 1995 to 2004, they were primarily in the B2B space selling tech to large corporates, especially in FMCGs like Coca-Cola and Marico. In 2004 they launched their consumer internet mapping platform.

Building a consumer-facing digital map is a tough business and it took them 10 years to cover a majority of the country.

The company currently earns the majority of its revenue from enterprise customers across three major categories — corporate, automotive, and government. In addition, MapMyIndia also offers professional-grade maps and products directly to retail customers through the Mappls app and GPS IoT-enabled gadgets and devices.

Today at Mcap of Rs 6,493 Cr, it’s trading at 26x TTM revenue (yes revenue) and just 72x TTM earnings thanks to its superior 38% of net margins.

If we just run by reverse DCF shown below -

To deliver a 15% cagr return to the investors the markets are expecting the company to grow by 25.5% cagr for the next 15 years with a terminal growth rate of 5%.

That means after 15 years company will trade at Mcap of 8 x 6493 = Rs 51944 /- which is not much but the real question is can it deliver a 25.5% cagr net profits growth for the next 15 years? and even if it does so how unfortunate it would be if investors just end up making 15% cagr.

clearly, the risk-reward isn’t really favorable on this investment. However, there are businesses like Bajaj Finance which have grown net profits 32% cagr in the last 10 years.

If MapMyIndia is able to do the same then it may be trading at a fair value today.

The problem with that is MapMyIndia’s 50% of revenue comes from the Auto sector and the Auto sector is cyclical which can of reflects in the revenue of MapMyIndia as between Fy18 to Fy 22 their revenue just grew by 7.5% cagr (thanks to their other 50% of the revenue that comes from Enterprise segment) but the great thing is despite that they were able to expand their margins and grew net profit by 25% cagr during this period and Now as the Auto sector reviving we can expect better revenue growth going forward.

Can they do the Bajaj Finance or Grow 30% cagr for the next 10 years?

To be able to understand this we have to understand the different revenue streams of the company ( how they make money) and hopefully understand the Moat around their business.

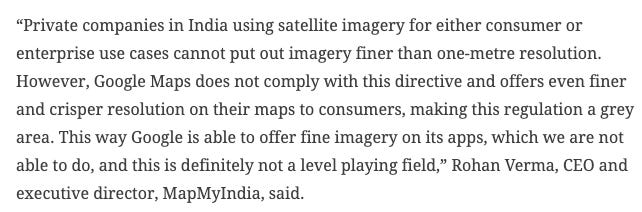

I often hear the question why Google Maps can’t do this? and I really don’t have the answer. Although the company claims they have better product offerings in B2B & B2B2C that’s why they win which really seems to be true and MapMyIndia enjoy the regulatory moat as well which is the restriction of foreign entities from collecting Map data but it looks like google has found a way to get around this regulation.

If America can use the satellite to spy on the Indian Nuclear testing site & Indian government despite knowing it couldn’t do anything about it then what’s stopping Americans to use satellites to map the whole of India with very finer details?

And I think that’s where google map has the advantage over MapMyIndia. To put it simply, google-map maps out the world with the combination of data collected and processed by satellites, government agencies, Google employees, and well, you.

Whereas MapMyIndia has collected its data literally by physically surveying the area using the sophisticated vehicle shown below -

MapMyIndia management counts this as their Moat because the company has been collecting data for about 30 years (for any new player it’s hard to gather this much data quickly). The company initially built the digital footprint of the available offline maps. Later, they physically surveyed the area, visiting different parts of the country.

In the past 30 years, they have successfully built a repository of more than two crore data points, including navigation systems, telematics, and 3D data visualizations.

It claims to have mapped more than 10.77 million distinct locations (Points of Interest), carried out coverage of more than 2.20 million kilometers of roads, 7,268 cities at the street level with home address level data for 94 cities, and 5.79 lakh villages.

When management says that it’s a moat that nobody new can trace the whole country quickly to be able to give the same offerings MapMyIndia is offering. I get it but it’s not necessarily true as anyone like google can use Satellite to map the country maybe the same offerings as MapMyIndia does? It’s another thing that no one would want to compete with google maps as google has real-time feedback from the folks like you and me to update its map in real-time as well with double confirmation from satellite data as well.

If GOI builds a new tunnel or an overbridge somewhere it’s google-map which will be able to come up quicker than MapMyIndia due to its superior data collection methodology as it uses a combination of data collected and processed by satellites, government agencies, Google employees, and you.

MapMyIndia recently has done a tie-up with Isro which may enable them to collect satellite data as well. Although Vehicle based mapping provides better accuracy and 3-D mapping for MapMyIndia but google street views aren’t that bad as well isn’t it?

so, on Moat, I don’t really think MapMyIndia has any over Google Maps, or at least I am not convinced as much as markets are convinced by it (trading at 26x TTM revenue, 70 PE). Infact if at all anyone has any moat is Google and one could argue why can’t google be able to Map India in 3D from space efficiently and in real-time given due to so much advancement in image tech that today we can even look into outer galaxies from space.

but it is also the fact that in the B2B segment MapMyIndia dominates the market share, why is it so? A) I think because that’s how this company started, During late 1990’s they bagged Coca-Cola as their first client to build a digital map for them that could solve their transportation problem in India. They later tied up with Cellular One and other companies to solve their respective problems related to topography and demography. These companies also funded the founders to solve their problems.

So, as they were solving a lot of enterprise problems they kept building for it and as the world became more and more digital MapMyIndia build more SDKs and APIs for other enterprises to seamlessly plugin their solutions built by the company and on the other hand google map remained uber focused on solving B2C market and that’s where google dominates today.

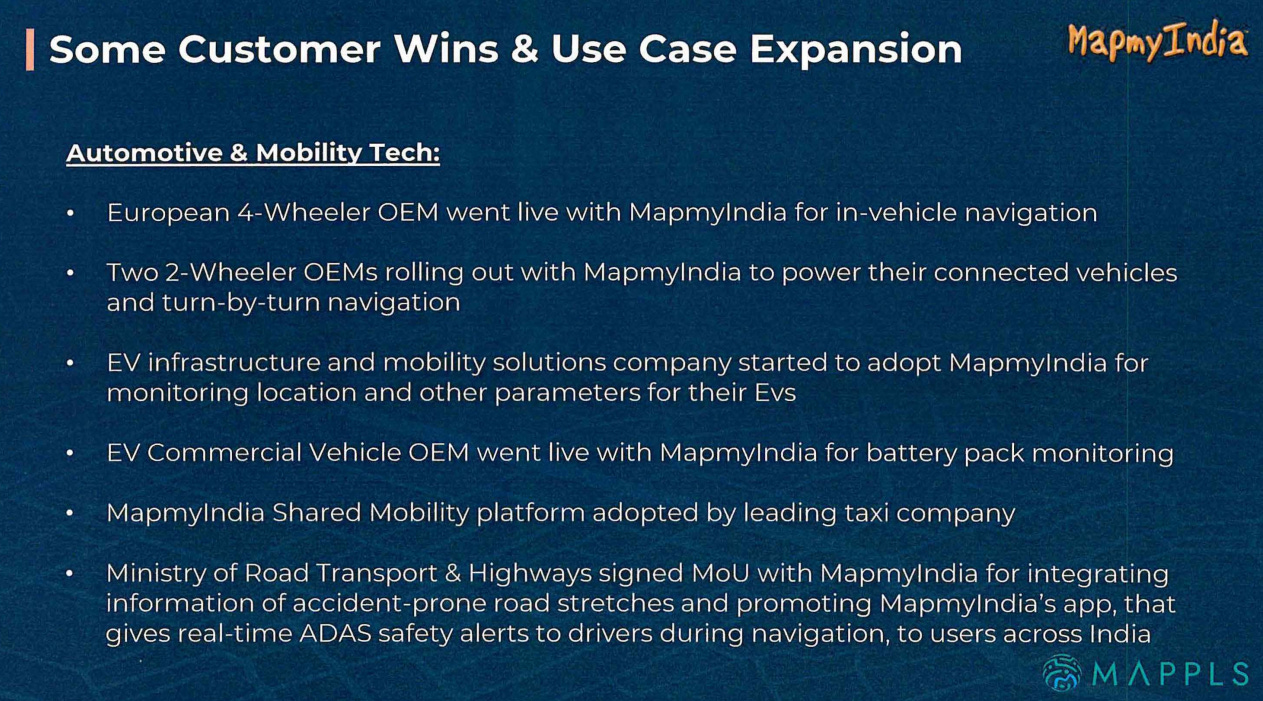

So today MapMyIndia For example to FMCG companies offers services including distribution analytics, field sales monitoring, safety mapping for long-distance routes, consumer location insights for marketing, and more. For telecom and utilities, it provides RF and optical fiber mapping, field force monitoring, line of sight analysis for 4G/5G planning and other services. Similarly, its services spread across logistics, retail, health and pharma, financial and other sectors. like here are some recent wins by the company in B2B / B2B2C space -

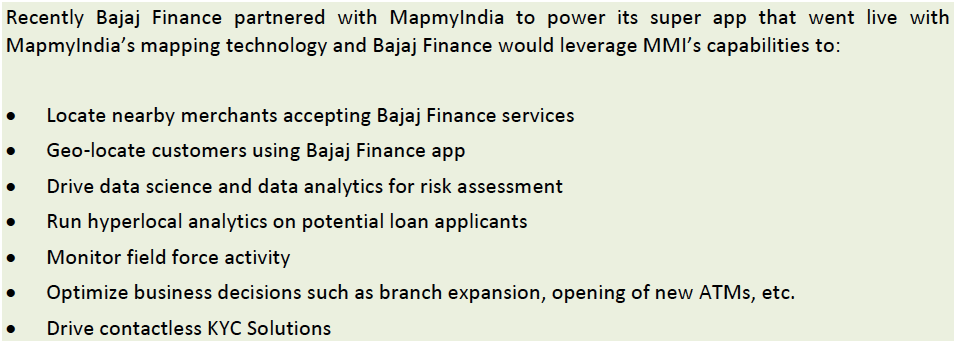

Here management explained why bajaj finance bought their services

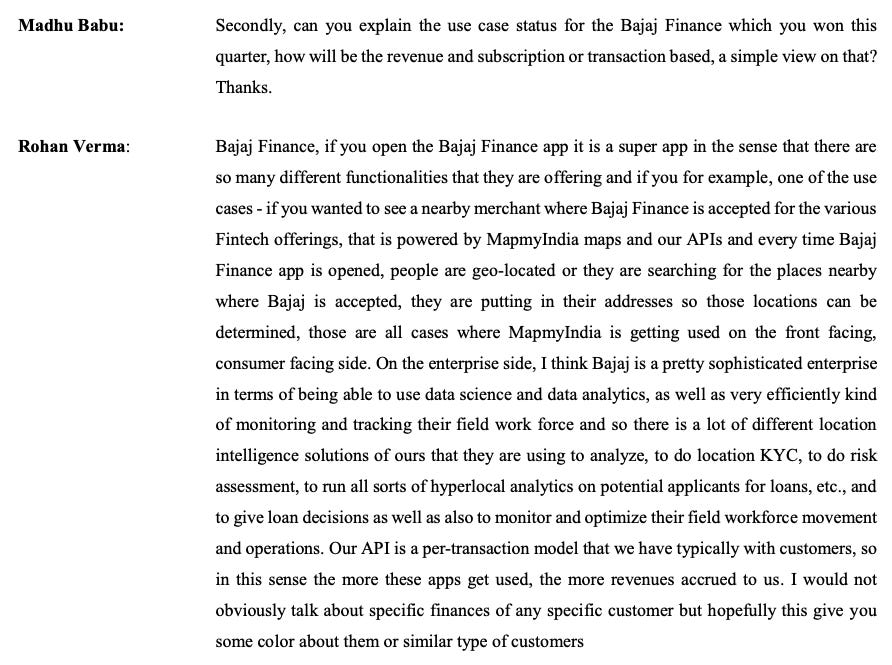

Some other snippets from the conf calls -

So one thing which is clear from the conference call snippets is that apart from mapping solutions MapMyIndia provides a whole lot of different software suit like analytics, IOT, Monitoring, workforce management, etc.

Whereas to compete with MapMyIndia in B2B space google-map has to work on all of these apart from what they do already.

One Moat for sure is there for MapMyIndia is that because they have built so many tailor-made solutions for their B2B clients it’s really hard for their clients to switch to other service providers.

The most beautiful thing about this B2B business is (that I think even markets as well appreciate today given the rich valuation) it’s really very underpenetrated in every other vertical they are present in.

like in financials HDFC and Bajaj finance are using it but can we imagine all financial services businesses start using it eventually? , same for FMCG, Auto, QSRs, Logistics, Proptech, Various Gov organizations etc, and on top of that new emerging sectors like Drones, Metaverse, etc could open up a new very large market for them.

Certainly due to the Atmnirbhar Bharat scheme, a lot of Government related business is coming to MapMyIndia and if you look globally Government plays a huge role. The trend has been Gov drive the 40% of the revenue for map providers. In India, this section has just picked up in the last two years. MapMyIndia bagged contracts from ISRO, Ministry of road transport, Civil Aviation, Cowin, GST dept, etc recently.

So, it does look like the market penetration for sure will drive decent growth for the company. For example, India has around 20 Cr registered vehicles today and given Ola electric putting it into their two-wheelers and Hyundai putting it in their 4 wheelers so, one can work with by 2040 all Vehicles on street might be running with the inbuilt navigation app.

Today let’s say 5% of Automobiles (2/3/4 wheelers) have an inbuilt navigation system and in 15 years let’s say all will start coming with an in-built navigation system. This is 20x growth from 5% to 100% (The auto sector may itself grow by 7-10% cagr this we are ignoring to be on the very conservative side of guestimate).

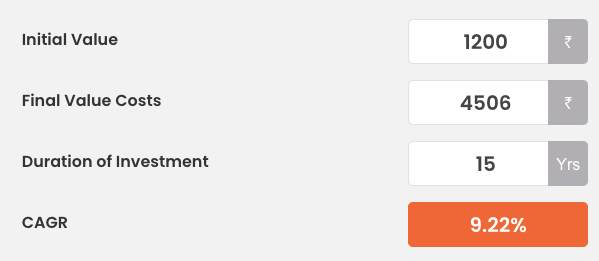

Today they do about Rs 100 Cr of sales from the Auto segment, so by 2035, they will end up doing Rs 2000 Cr sales from Auto alone. Let’s say that today the Enterprise segment also contributes the other 50% of the revenue which is Rs 2000 Cr.

Total sales by 2035 Rs 4000 Cr, 40% net margins means Net profit by 2035 will be

Rs 1600 Cr, which translates into EPS of 280.00 by Fy 2035, and if do our fav DFC by keeping moderate future growth expectation beyond Fy35 with 15% discount rate.

We get Rs 4,506 /- the per-share value of the company in Fy35, which really translate into 9.2% cagr return.

I can be wrong in many ways as it’s really hard to think about by how much Enterprise revenue will grow, will it grow faster than Auto or the same or slower than auto? that we can’t estimate. Today revenue is split between auto and enterprise 50-50% that’s what we took.

The whole idea about the above exercise was just to see if even if we grow Auto and Enterprise revenue by 20x in 15 years it’s still not trading at fair value.

Inorganic growth -

I liked their acquisition of Gtropy

Already about Rs 24 Cr (16%) of the H1 Fy23 revenue of MapMyIndia is coming from Gtropy and Gtropy is growing at a decent rate (>20%).

Today they have about Rs 400 Cr of cash which they are using to make these kinds of acquisitions in their sector. so, huge value creation could happen if they end up buying an even better business than what they have today at a very early stage.

Without a doubt, it’s a great business and has a long runway for growth but unfortunately, most of the future growth is already priced in, I may think about buying it at the range of Rs 800 - Rs 900 if ever it’s going to trade there, As the risk-reward around price Rs 800-900 /- is much much better than what it’s offering today.

Good insight

As usual Nice write-up Dhruva. In comparison with Google Maps I would agree they don't have a moat on the technology front, but otherwise I believe they have an advantage in trust (Similar to Buffet and Embracer Group (Nordstern Q3FY21 for better understanding)) where the companies don't trust Google for being Google, Auto companies for their own Autonomous vehicles and Govts, for their anti-competitive nature. C.E. has advantage in both these cases where they have trust of early backers that they wont cross the line along with allied services like Bajaj Finance, and also a homegrown player helps in government showing a good face. But I also believe their competitors could be companies like Esri which are used by Amazon but not a direct subsidiary.