John Cockerill India Ltd: A Value Investment Analysis

Introduction: The Philosophy of Intrinsic Value and Market Delusions

In the disciplined pursuit of value investing, one must rigorously adhere to a foundational principle: a share of stock is not an electronic blip on a trading screen, nor is it a vehicle for macroeconomic speculation or a ticket to participate in the latest thematic market frenzy. Rather, it represents a fractional ownership interest in an underlying, living business enterprise. The rational investor’s solitary objective is to evaluate the economic characteristics of that specific enterprise, assess the durability of its competitive advantages, evaluate the competence and integrity of its management, and ultimately determine its intrinsic value—defined as the discounted present value of the cash that can be extracted from the business over its remaining life. Only when the market price of the equity is quoted at a significant discount to this conservatively calculated intrinsic value does an investment opportunity exist. This discount is the “margin of safety.”

When turning the analytical lens toward John Cockerill India Ltd (JCIL), the publicly listed Indian subsidiary of the venerable Belgium-based John Cockerill Group, an investor is immediately confronted with a fascinating and dangerous dichotomy. Over the past several years, and accelerating into 2026, the capital markets have exhibited an overwhelming, almost manic enthusiasm for the company. This exuberance has driven the company’s share price to extraordinary, stratospheric multiples, untethered from the historical earning power of the firm. To understand this phenomenon, one must recognize that the market operates as a voting machine in the short term, heavily influenced by narratives. In the case of JCIL, the narrative is powerfully tethered to the broader global pivot toward decarbonization, “green steel,” and the emerging, heavily subsidized hydrogen economy.

However, as Charlie Munger has often advised, one must invert the problem to truly understand it. The intelligent investment framework requires looking past the glossy headlines of green hydrogen gigafactories and examining the cold, hard cash-generating realities of the listed Indian operation. What is the business actually doing today? How much capital does it require to operate? How much cash does it return to its owners? And most importantly, are the lucrative green energy cash flows that the market is salivating over actually accruing to the minority shareholders of this specific listed entity?

The ensuing report provides an exhaustive, multi-layered examination of John Cockerill India Ltd. It scrutinizes the company’s traditional engineering and capital goods operations, interrogates the true nature of its exposure to the green hydrogen sector, dissects its economic moat (or lack thereof), evaluates its corporate governance, and assesses its capital allocation framework. The report culminates in a rigorous assessment of its valuation, contrasting the market’s euphoric pricing against the sober reality of its intrinsic value.

The Circle of Competence: Understanding the Core Economic Engine

To predict the long-term economics of any business, one must first operate strictly within a defined “circle of competence.” This requires a granular understanding of how the company operates, how it serves its customers, the nature of its products, and the structural, macroeconomic dynamics of the industry in which it resides. John Cockerill India Ltd operates at the intersection of heavy industrial engineering, capital goods manufacturing, and steel infrastructure.

The Legacy Operations and the EPC Business Model

Incorporated in 1986 under the name Flat Products Equipment India Ltd, the company was assimilated into the Belgium-based John Cockerill Group in 2008. Today, JCIL serves as a premier engineering and technology entity, acting as a strategic hub for the parent group’s operations in Asia and employing over 400 individuals in India.

The core operations of the company revolve around the bespoke design, engineering, manufacture, and installation of complex equipment for the ferrous and non-ferrous industries globally. The product portfolio is highly specialized and heavily reliant on the capital expenditure (capex) budgets of massive industrial conglomerates. JCIL’s offerings encompass several critical categories:

First, the company is a dominant force in Cold Rolling Mill Complexes. These massive installations are essential for processing hot-rolled steel into thinner, more refined cold-rolled steel, which is subsequently used in high-value applications such as automotive manufacturing, home appliances, and advanced construction.

Second, JCIL designs and commissions intricate Processing Lines. These include continuous galvanizing lines (CGL), pickling lines, color coating lines, and specialized processing lines for stainless steel and aluminum. A prime example of this operational segment is the recent large-scale Continuous Galvanizing Line order secured from JSW Steel, valued between INR 4.4 billion and INR 4.7 billion. This single order will act as a primary revenue driver for the company over the subsequent three years.10 Similarly, the company secured a significant order of approximately INR 13 billion (INR 1,300 Crores) from JSW Vijayanagar Metallics for commissioning two annealing and coating lines.

Third, the company operates an Industrial Boilers and Thermal Treatment division. This segment provides heat recovery steam generators (HRSG), waste heat recovery systems, and industrial utility boilers aimed at optimizing plant operations, capturing waste heat, and reducing overall industrial energy consumption.

Finally, JCIL provides specialized Chemical Equipment, including facilities for acid regeneration and associated environmental air and water treatment technologies.

This business model is fundamentally categorized as Engineering, Procurement, and Construction (EPC) coupled with Original Equipment Manufacturing (OEM). In evaluating the economics of EPC businesses, a value investor must recognize their inherent limitations. These businesses are capital-heavy, fiercely competitive, and exceptionally cyclical. They are deeply tethered to the macroeconomic capex cycles of the global and domestic steel industries. When steelmakers are profitable and expanding—often driven by infrastructure booms or protectionist trade policies—order books swell. Conversely, when the global commodity cycle turns, capital goods providers suffer severe and immediate earnings compressions.

The Strategic Pivot Toward Value Services

Historically, large-scale EPC and heavy engineering businesses suffer from structurally low margins. This is due to intense competitive bidding processes where sophisticated buyers squeeze suppliers, combined with the omnipresent risk of cost overruns, raw material inflation, and execution delays during prolonged multi-year timelines. Recognizing this structural economic limitation, JCIL’s management has articulated a strategic pivot aimed at improving the quality of its earnings.

The company is actively attempting to increase its “Value Services” mix. Presently, the management is targeting an expansion of its high-margin services, maintenance, spare parts, and upgrading business to represent approximately 30% to 35% of total consolidated revenue over a three-to-five-year horizon.

In the framework of business economics, transitioning a substantial portion of revenue from lumpy, low-margin project execution to predictable, high-margin service contracts is a highly rational strategy. Unlike massive capital projects—which take upwards of three years to execute and consume vast amounts of working capital—value services and spare parts orders provide recurring revenue, execute in vastly shorter cycles of 12 to 18 months, and require minimal incremental capital investment.10 By increasing the velocity of capital and improving operating margins, this structural lever is designed to lift the company’s overall Return on Invested Capital (ROIC), which has historically been lackluster.

Furthermore, JCIL is attempting to localize specialized capabilities to improve customer turnaround times. For instance, the company is preparing to commission a Rolls Coating Facility in Taloja, dismantling old assets to create space for localized, specialized coating capabilities that were previously outsourced or delayed.

The Green Hydrogen Illusion: Separating the Parent from the Subsidiary

The most critical element in analyzing JCIL today—and the primary reason the stock has experienced such explosive price appreciation—is the market’s profound misunderstanding of the company’s actual exposure to the green hydrogen economy. A rigorous investment analysis requires disentangling the market’s perception of the listed entity’s “Green Hydrogen” capabilities from the unyielding operational realities of its corporate structure.

The capital markets have rewarded JCIL with a staggering valuation premium, largely because the parent company, John Cockerill SA (headquartered in Seraing, Belgium), is an undisputed global leader in pressurized alkaline electrolyzer technology and green hydrogen infrastructure.

The Parent Company’s Hydrogen Dominance

The unlisted parent entity is indeed a formidable player in the global energy transition. It holds an estimated 85% market share in global alkaline electrolyzer sales.13 The parent company offers a wide range of electrolyzers, from small-scale units to massive 1000Nm³ per hour (5MW) systems, which are currently among the world’s most powerful.

In India, the parent group has made massive, highly publicized strides. John Cockerill Hydrogen forged a strategic joint venture partnership with Indian renewable energy giant Greenko (now operating under the AM Green umbrella) to establish a 1 GW electrolyzer gigafactory in Kakinada, Andhra Pradesh, with stated plans to scale this capacity to 2 GW by 2029.

This Kakinada facility has already secured monumental orders. Most notably, AM Green Ammonia placed a 1.3 GW order with John Cockerill for what will be a one-million-tonne green ammonia project in Kakinada, slated for production in the second half of 2026.16 This project is supported by a Production Linked Incentive (PLI) allocation for 300 MW annually, cementing the group’s position as a key beneficiary of India’s National Green Hydrogen Mission.

Furthermore, to fund this explosive growth, the global John Cockerill Hydrogen business recently completed a €116 million capital raise involving major strategic and industrial investors, including the Belgian infrastructure group Fluxys, SLB, SFPIM, Wallonie Entreprendre, and Rely (a joint venture between Technip Energies and John Cockerill).

The Reality for the Listed Subsidiary (JCIL)

A superficial analysis—which appears to be exactly what the broader retail and momentum-driven market has conducted—leads to the assumption that John Cockerill India Ltd (the publicly traded listed entity on the BSE and NSE) is the primary economic beneficiary of the Kakinada gigafactory and the broader electrolyzer boom in India. This assumption is fundamentally and demonstrably flawed.

During the May 2026 earnings conference call, JCIL’s Chairman provided absolute clarity on this exact subject, shattering the retail narrative for those who cared to read the transcript. When directly asked if the listed Indian entity (JCIL) would manufacture components for the massive green hydrogen electrolyzer project signed between the parent group and Greenko/AM Green, the management explicitly stated that JCIL remains fundamentally focused on the steel industry.

The hydrogen business operates as an entirely separate corporate entity within the broader global John Cockerill Group.20 Manufacturing pressurized alkaline electrolyzers requires highly specific, specialized, and asset-intensive setups that are currently localized in the group’s established facilities in France (Aspach) and China, and will eventually be housed in the new Indian joint venture facilities.

Consequently, JCIL is not in a position to manufacture components for these electrolyzers out of its existing facilities, such as the Taloja workshop.

While the parent group intends to build dedicated manufacturing capacity in India (Kakinada), the cash flows, profit margins, and intrinsic economic benefits of those specific electrolyzer sales accrue directly to the private joint venture (AM Green and John Cockerill SA) and the unlisted parent company. They do not flow down to the income statement or balance sheet of the listed JCIL entity. Investors purchasing JCIL stock today at 150 times earnings in the belief that they are buying India’s premier electrolyzer manufacturer are participating in a grand delusion.

JCIL’s True, Nuanced Exposure to Decarbonization

This is not to say that JCIL is entirely isolated from the decarbonization megatrend. Its involvement, however, is deeply rooted within its traditional circle of competence: the legacy steel industry. JCIL is approaching the green transition through two distinct, highly specialized avenues:

First, in the realm of Downstream Hydrogen Combustion: Within its existing Services & Energy Efficiency segment, JCIL is actively retrofitting and upgrading downstream steel furnaces to utilize hydrogen combustion. This assists legacy, high-emission steel manufacturers in decarbonizing their existing assets and optimizing plant operations without requiring wholesale replacement of their infrastructure.

Second, through Upstream Green Steelmaking Technologies: JCIL is attempting to expand into upstream steel manufacturing processes. This includes the development and deployment of Direct Reduction Iron (DRI) solutions that utilize hydrogen fuel instead of highly polluting coking coal.7 Furthermore, the company is deeply involved in a revolutionary technology platform known as “Volteron.” This disruptive process utilizes low-temperature iron electrowinning in an aqueous electrolyte to transform iron oxide directly into steel plates, completely bypassing the traditional, carbon-intensive blast furnace. A pilot project, with intellectual property shared between ArcelorMittal and John Cockerill, aims to produce 200,000 tons of annual iron plates via this method by 2027.

Additionally, JCIL has signed a strategic Memorandum of Understanding (MoU) with the Steel Authority of India Limited (SAIL). This collaboration focuses on integrating green hydrogen into iron and steelmaking processes, and crucially, setting up a massive downstream plant for cold-rolled grain-oriented (CRGO) and cold-rolled non-oriented (CRNO) electrical steel. This joint venture, representing an investment of nearly INR 6,000 crores, is slated to begin operations between 2027 and 2029 with a production target of 1.5 million tonnes per year.

The distinction here is paramount to the valuation thesis: JCIL is a provider of decarbonized steel processing equipment, not a manufacturer of hydrogen electrolyzers. The market’s failure to distinguish between the parent’s green hydrogen gigafactory and the subsidiary’s steel-focused EPC operations has created a severe pricing distortion.

The Elusive Economic Moat and the Competitive Landscape

A durable competitive advantage—frequently conceptualized as an “economic moat”—is the defining characteristic of an exceptional business. It allows a company to maintain high returns on invested capital over long periods, resisting the gravitational pull of competition that typically erodes outsized profits. Moats generally arise from low-cost production advantages, high customer switching costs, powerful network effects, or unique intangible assets such as strong consumer brands, patents, or strict regulatory licenses.

The Structural Reality of the Capital Goods Sector

JCIL operates in the industrial machinery and capital goods sector. Historically, this industry is characterized by the near-total absence of an economic moat. Capital equipment, ranging from continuous annealing lines to waste heat recovery boilers, is purchased by highly sophisticated, entirely rational corporate buyers (e.g., JSW Steel, Tata Steel, AMNS, SAIL) who utilize rigorous, multi-stage competitive bidding processes.

Competitors in this specific industrial space—such as SMS Group, Danieli, Tenova on the global stage, alongside domestic players like ISGEC Heavy Engineering, L&T Heavy Engineering, Thermax, and Elecon Engineering—are equally capable of delivering complex, bespoke engineering solutions. In a highly fragmented competitive bidding environment where capital is abundant and technical engineering expertise is relatively commoditized among a few global oligopolists, the supplier capable of offering the lowest cost, or the most generous financing terms, often wins the contract. This fundamental dynamic strips away pricing power and structurally depresses profit margins across the industry.

Intangible Assets: The “Rented” Technological Umbrella

If JCIL possesses any semblance of an economic moat, it is derived entirely from its intangible assets—specifically, the immediate technological transfer from its parent, John Cockerill SA. The 200-year legacy of the parent group provides the Indian subsidiary with instant access to proprietary, globally tested designs for high-efficiency processing lines, chemical recovery plants, and next-generation coating technologies.

For example, the group’s proprietary Jet Vapor Deposition (JVD) technology offers a high-efficiency, lower-environmental-impact coating alternative that is incredibly difficult for purely domestic Indian competitors to replicate without undertaking massive, multi-year R&D expenditures.10 By acting as the localized Indian hub, JCIL benefits from global technological breakthroughs without bearing the entirety of the financial risk associated with research and development.

However, an intelligent investor must recognize that this technological moat is essentially “rented” rather than “owned.” Access to this proprietary technology, global brand recognition, and engineering blueprints comes at a direct, recurring cost to JCIL’s minority shareholders. This dynamic leads directly to an examination of corporate governance and the mechanisms of capital extraction.

Corporate Governance, Management, and The “Toll Bridge”

In evaluating a business enterprise, the integrity, transparency, and capital allocation skills of the management team are of equal importance to the underlying economics of the business model. When investing in a publicly listed subsidiary of a massive multinational corporation, one must apply heightened scrutiny to the relationship between the parent and the subsidiary. The primary risk in such structures is that economic value is disproportionately siphoned upward to the parent entity, leaving the domestic minority shareholders with sub-par returns.

Promoter Holding and the Absence of Institutional Oversight

John Cockerill SA (the parent) currently maintains a commanding 70.44% promoter ownership stake in JCIL. This level of control dictates the strategic direction of the company without meaningful opposition. Furthermore, the shareholding pattern reveals a striking lack of institutional sponsorship. Foreign Institutional Investors (FIIs) hold a negligible 0.02%, and Domestic Institutional Investors (DIIs) hold exactly 0.00% of the equity. The remaining 29.54% float is held entirely by the retail public. The absence of sophisticated institutional investors often removes a critical layer of external governance pressure and analytical rigor, allowing momentum-driven retail speculation to dictate the share price.

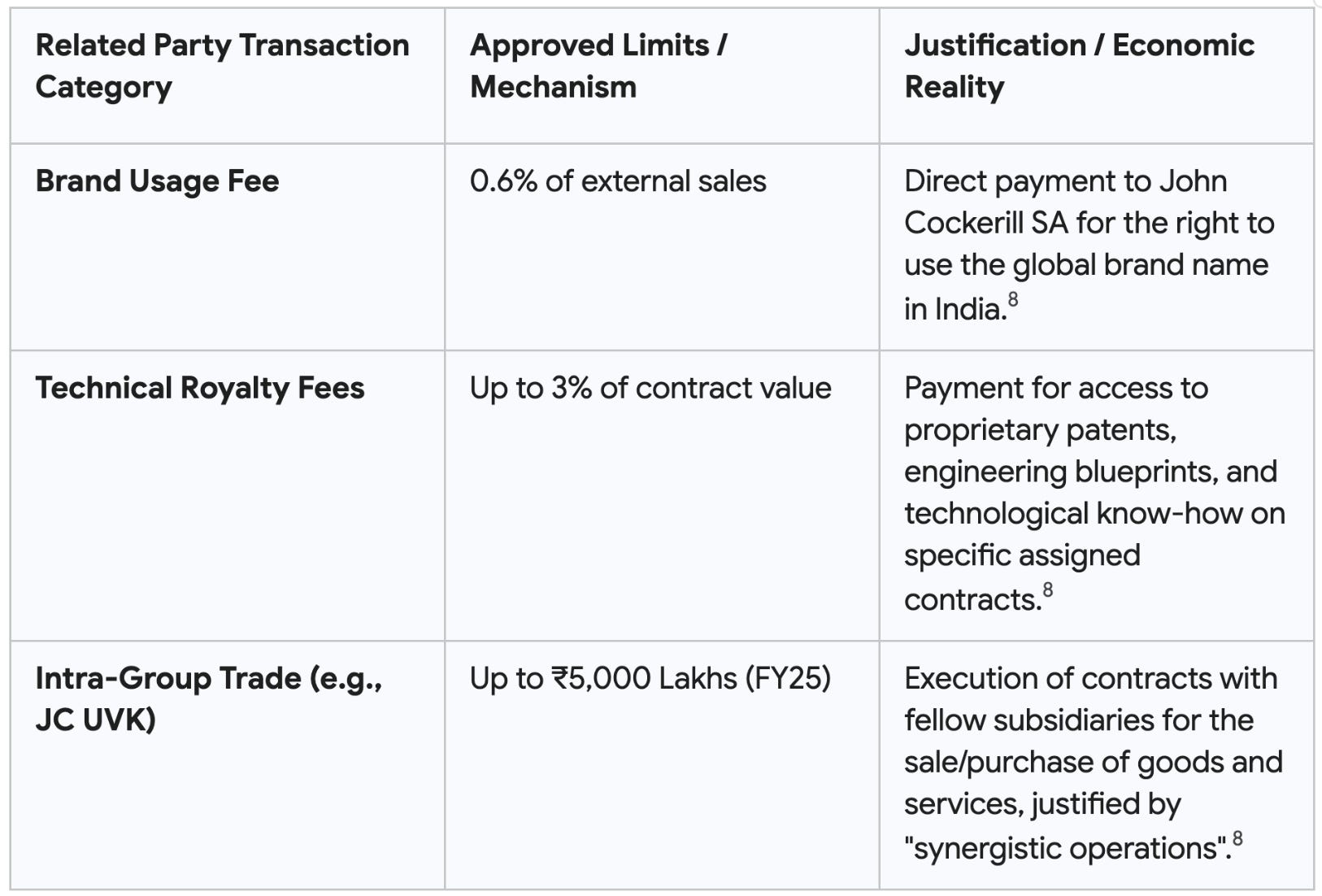

Related Party Transactions (RPTs): The Architecture of Extraction

The most critical area of governance analysis for JCIL involves Related Party Transactions (RPTs). JCIL relies heavily on its parent and fellow global subsidiaries for technology, design engineering, brand equity, and cross-border project execution. A detailed review of the 2024 and 2025 Annual Reports reveals a web of material financial arrangements with the parent entity that structurally limit the profitability of the listed Indian firm.

According to regulatory filings, JCIL seeks shareholder approval for several specific, recurring payments to John Cockerill SA and its affiliates:

While these royalty and brand fee arrangements are entirely legal and represent standard operating procedure among multinational subsidiaries operating in India, they act as a financial “toll bridge.” In a business that historically struggles to generate operating margins above 5%, stripping away up to 3.6% of top-line revenue (0.6% brand + 3% royalty) before accounting for local operational expenses is a massive structural impediment. Every rupee paid in top-line royalties is a rupee permanently removed from the operating profit available to minority shareholders.

The Board maintains strict legal compliance, ensuring these material RPTs receive omnibus approval from the Audit Committee and are ratified by shareholders as per SEBI listing regulations. However, compliance does not negate the economic reality: the parent company possesses an incentive-caused bias to extract value via guaranteed top-line royalties rather than relying on bottom-line dividend distributions, which must be shared with the 29.54% retail base.

Capital Allocation, Solvency, and the Balance Sheet

A business generates intrinsic value through a combination of two activities: generating cash from its existing operations, and reinvesting that cash at high rates of return. If a company cannot reinvest its retained earnings at rates exceeding its cost of capital, it is duty-bound to return that capital to its owners via dividends or share repurchases.

A Fortress Balance Sheet

From a balance sheet perspective, JCIL’s management deserves immense credit for demonstrating exceptional fiscal conservatism. Capital goods businesses are inherently volatile, characterized by dramatic swings in revenue. Utilizing financial leverage (debt) in a highly cyclical industry is a classic recipe for permanent capital impairment.

JCIL operates as a virtually debt-free enterprise. As of the most recent filings, the company maintains total shareholder equity of approximately ₹2.10 billion (₹210 Crores) against a negligible total debt of ₹53.2 million (₹5.32 Crores).1 This results in a pristine, highly conservative debt-to-equity ratio of 2.5%. Furthermore, the company holds robust liquidity, with cash and short-term investments totaling ₹2.27 billion (₹227 Crores), providing an interest coverage ratio of 3.9x based on recent EBIT figures.

This unlevered balance sheet ensures the company’s survival through the inevitable troughs of the steel capex cycle. It allows JCIL to fund its ongoing operations and working capital requirements entirely through internal accruals, without being at the mercy of credit markets during liquidity crunches.

The Working Capital Drag and Poor Capital Returns

However, despite being debt-free, the business is exceptionally capital-hungry due to structural working capital inefficiencies inherent to the EPC industry. A stark metric highlights this vulnerability: JCIL suffers from exceptionally high debtor days, recently reported at an alarming 212.89 days.29

In the heavy EPC industry, capital routinely gets tied up in long-term receivables, unbilled revenue, and customized inventory. When a company takes over 200 days to collect cash from its clients (even highly solvent ones like Tata Steel or JSW), it severely depresses the conversion of accounting profits into actual free cash flow. A business that reports accounting profits on the income statement but continuously consumes cash to fund an ever-expanding pile of receivables is fundamentally less valuable than one that generates surplus, distributable free cash flow.

This inability to efficiently cycle capital is reflected in the company’s historical return metrics. Over the last three to five years, the Return on Equity (ROE) has languished in the mid-single digits, generally resting between 4.38% and 5.02%.29 The Return on Capital Employed (ROCE) has similarly hovered between 6.23% and 7.00%.29 When a business earns 5% on its equity capital in an environment where the risk-free rate of a government bond exceeds 7%, it is destroying, not creating, economic value.

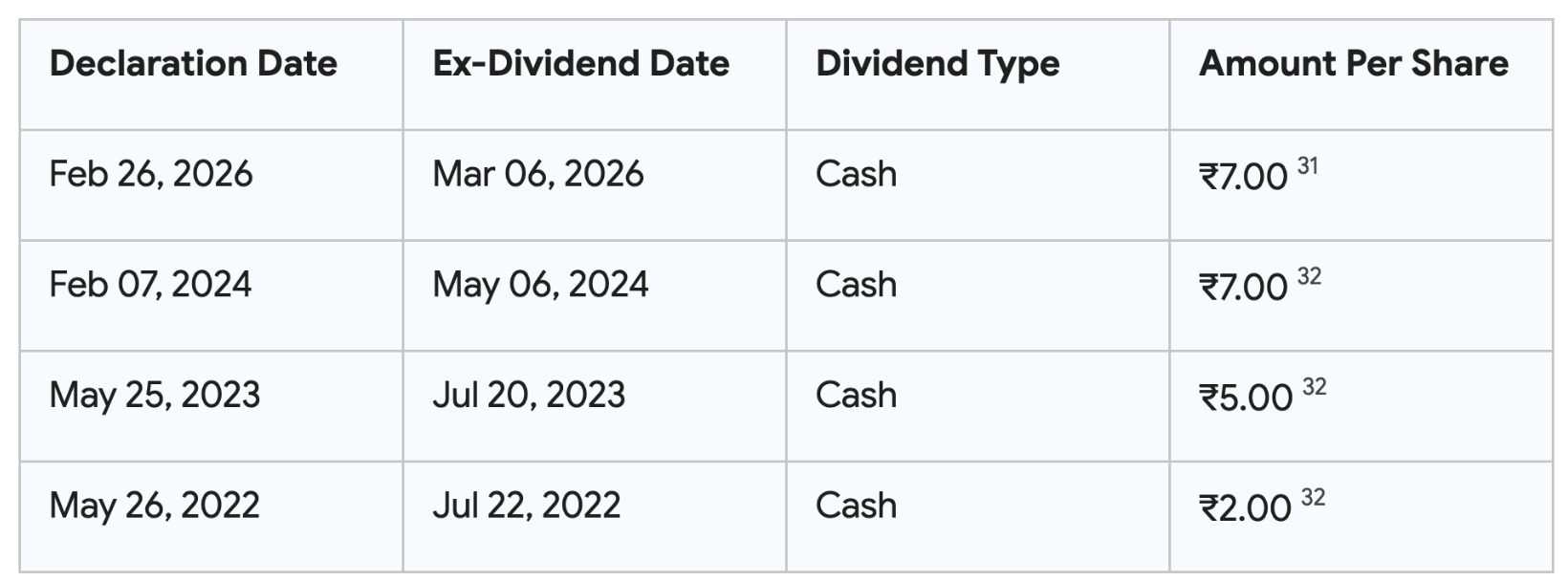

Dividend Policy

Because the business struggles to reinvest capital at high rates, it maintains a policy of distributing dividends to shareholders. The company has a history of sporadic, yet somewhat consistent, dividend payouts.

While a ₹7.00 dividend per share sounds positive, one must contextualize it against the prevailing market price of the equity. At current market prices (ranging from ₹5,400 to over ₹9,000 depending on the recent trading week), this absolute payout translates to an anemic dividend yield of approximately 0.08% to 0.14%. Investors are receiving practically no yield to wait for the business to improve.

Historical Earning Power and Operating Dynamics

A comprehensive assessment of a company’s earning power requires analyzing its financial performance across a full economic cycle, observing how it performs in both expansionary and recessionary environments, rather than linearly extrapolating from a single record quarter.

The Erratic Trajectory of Revenue and Earnings

JCIL’s financial history over the last five to ten years perfectly encapsulates the feast-or-famine nature of the capital goods sector. The income statement resembles a roller coaster, highly dependent on the timing of massive project completions.

FY2021: Operating in the shadows of macroeconomic slowdowns, the company reported a severe net loss, with an EPS of -₹58.86.

FY2022: As global capex recovered post-pandemic, JCIL returned to profitability, generating ₹3.89 billion in revenue and ₹46.4 million in net income, resulting in an EPS of ₹9.40.

FY2023: Strong project execution led to substantial revenue growth to ₹4.84 billion. Net income surged to ₹128.9 million, resulting in an EPS of ₹26.10, with profit margins expanding to 2.7%.1

FY2024: The inherent lumpiness of the EPC model struck again. The company reported a massive revenue decline of 56% to ₹3.89 billion and slumped back into unprofitability, posting a net loss of ₹53.8 million (EPS loss of ₹10.90). Management attributed this contraction to cyclical headwinds in domestic order inflows and delays in finalizing key projects.

FY2025 (TTM): A significant financial turnaround materialized as delayed orders commenced execution. The company reported a Profit After Tax (PAT) of ₹103.1 million (₹10.31 Crores) on revenues of ₹3.57 billion. The TTM EPS rebounded to ₹20.89, yielding a modest net profit margin of 2.8%.

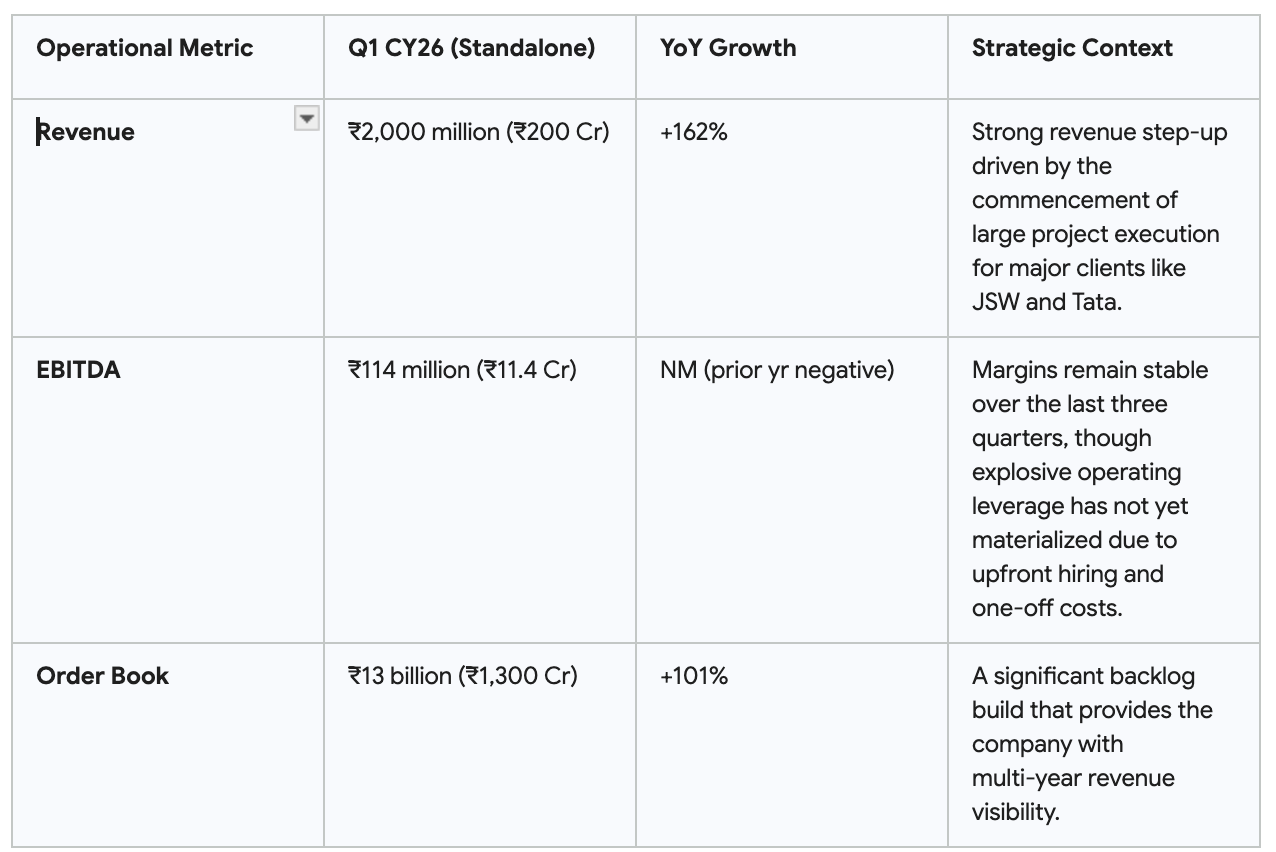

The Recent Inflection: Q1 CY26 Results and Global Consolidation

The most recent data from the quarter ending March 2026 (Q4 FY26) suggests a potential structural inflection point in operations, driven by a massive, concerted build-up in the order book.

Furthermore, the Q1 CY26 consolidated revenue was reported at a robust ₹3.4 billion (₹340 Crores), an increase of 56% YoY. Crucially, management noted that the first quarter of CY26 represented the first consolidated quarter that includes operations integrated from China, Belgium, and Germany. This geographic and operational consolidation fundamentally alters the scale of the entity reported to Indian shareholders. However, the exact integration mechanics, the cultural challenges of cross-border consolidation, and the long-term margin implications of absorbing these overseas units will require intense monitoring in future quarters.

The Margin Profile Challenge

The core vulnerability of JCIL has always been its razor-thin operating margins. Operating Profit Margins (OPM) have historically hovered in the low single digits (e.g., 0.28% to 1.43%), often falling into negative territory during revenue downturns.

During recent communications, management has targeted a consolidated EBITDA margin trajectory of “more than 10% over the next three years”. This step-by-step improvement is theoretically predicated on the execution of higher-margin orders booked in late CY25 and the aforementioned structural shift toward the Value Services segment. While a 10% EBITDA margin is theoretically achievable for a mature industrial services firm, the lack of operating leverage demonstrated to date—which management blames on upfront hiring costs and one-off consolidation expenses—suggests that realizing these gains will require flawless execution in an unforgiving macroeconomic environment.

Valuation: The Margin of Safety Test

The absolute cornerstone of prudent, intelligent investing is the concept of the Margin of Safety—the principle of purchasing a security at a price sufficiently below its conservatively calculated intrinsic value to allow for human error, bad luck, unexpected corporate developments, or extreme macroeconomic volatility. As Buffett frequently reminds investors: Price is what you pay; value is what you get.

Applying this framework to John Cockerill India Ltd reveals a deeply troubling scenario. The current market valuation of JCIL violates virtually every tenet of value-based pricing. The equity is currently priced not for a highly cyclical, low-margin, capital-intensive heavy equipment provider, but rather for an exponentially growing, high-margin, capital-light software or deep-tech franchise.

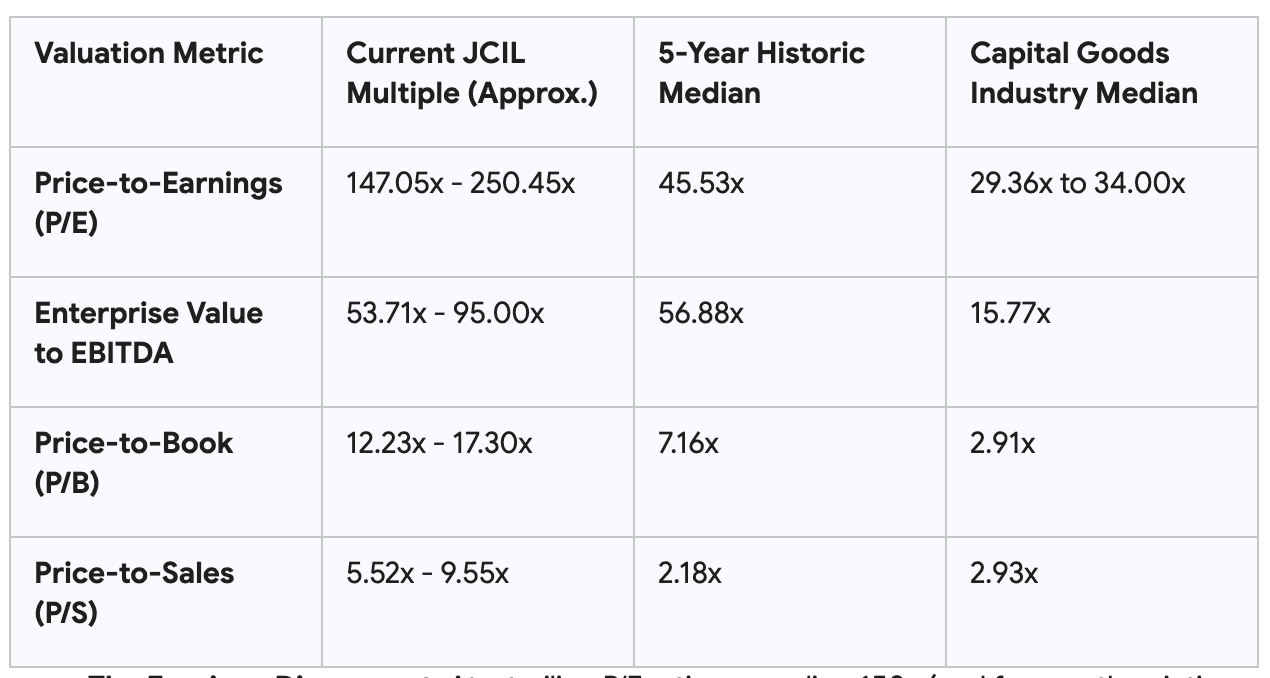

The Multiples Analysis: A Pricing Disconnect

Depending on the specific trading day and the latest momentum swings in the recent quarter, JCIL commands a market capitalization fluctuating between ₹45.24 billion (₹4,524 Crores) and ₹51.80 billion (₹5,180 Crores).6 When this market capitalization is juxtaposed against the company’s actual fundamental earning power, the resulting valuation multiples are exorbitant, bordering on the absurd:

The Earnings Disconnect: At a trailing P/E ratio exceeding 150x (and frequently printing over 200x during momentum spikes), investors are effectively willing to wait over a century and a half for the company’s current earnings to repay their purchase price.

The Book Value Disconnect: Paying 12 to 17 times book value for an enterprise that historically generates a 5% Return on Equity is mathematically irrational. It implies that the market is willing to pay 12 rupees to acquire 1 rupee of corporate equity that has proven capable of generating only 5 paise of annual return.

The Cash Flow Disconnect: An EV/EBITDA multiple of 95x is unprecedented for an industrial firm. A standard, mature, cash-generative industrial company typically trades between 8x and 12x EV/EBITDA.

Peer Comparison: The Reality Check

When evaluated against its domestic peers in the engineering and capital goods sector—companies such as Thermax, Cummins India, AIA Engineering, and Kirloskar Oil Engines—JCIL’s valuation appears radically disconnected from its fundamentals.

Consider a peer like Cummins India or Thermax. These companies exhibit far superior, double-digit Returns on Equity, possess robust and consistent free cash flow profiles, maintain established margin stability across economic cycles, and boast dominant, self-sustaining economic moats. Yet, they trade at significantly lower, more rational valuation multiples (typically in the 30x to 50x P/E range). The market is pricing JCIL as if it is a vastly superior business to its established blue-chip peers, an assumption that the underlying financial data flatly contradicts.

The Implied Growth Fallacy

To truly grasp the danger of the current valuation, an investor must utilize a reverse discounted cash flow (DCF) thought experiment. One must ask: What level of future cash flow generation is mathematically required to justify a ₹4,700 Crore valuation today?

Let us assume a highly optimistic, near-perfect execution scenario where JCIL successfully achieves its aggressive 10% EBITDA margin target, effectively doubling its current net margins to roughly 6%. Let us further assume the company sustains an uninterrupted 20% annual revenue growth rate for the next decade—a feat rarely achieved by cyclical EPC firms. Even under these heroic, flawless assumptions, the present value of those future cash flows, discounted at a standard 10% cost of equity, would struggle to justify even half of the company’s current market capitalization.

The reality is that “Mr. Market” is currently suffering from a severe thematic delusion. Investors are aggressively pricing into JCIL the exponential growth of the global hydrogen economy, the massive 1 GW electrolyzer gigafactory in Kakinada, and the multi-billion-dollar potential of the broader AM Green joint venture. However, as previously established by the company’s own management, those highly lucrative electrolyzer cash flows are captured by the unlisted parent entity and the private joint venture structures.20 They do not belong to JCIL. The listed entity is being awarded a “Green Energy Pioneer” multiple while remaining, at its core, a low-margin purveyor of cold rolling mills and steel processing lines that pays up to 3.6% of its top-line revenue back to its parent in royalties.

Expected Revenue Growth (5 Years from Now) Looking ahead to 2030 (roughly 5 years from the CY25 baseline), management has outlined highly ambitious growth aspirations.

Revenue Target: The management’s stated aspiration is to reach ₹8,000 crores (₹80 billion) in revenue by 2030.

Growth Drivers: This top-line growth is expected to be fueled by the global consolidation, India’s national push to achieve 300 MTPA steel production capacity by 2030, the commercialization of new technologies like Jet Vapor Deposition (JVD), and a strategic shift to expand the high-margin “Revamps, Spares & Services” business from its current levels to 30–35% of the total revenue mix over the next 3 to 5 years

From earning call Q4 Fy26 - Which made the stock go Bazooka

Here is a quick, high-impact breakdown of how JCIL is transitioning from a localized downstream firm into the centralized global anchor for the John Cockerill Group’s entire Metals division.

The Restructuring: Project Vulcain

The Deal: JCIL acquired 100% of John Cockerill Metals International (JCMI), absorbing the group’s engineering and sourcing arms across Europe, China, and the US.

Balance Sheet Optimization: To avoid negative equity under Ind AS, the board slashed the purchase consideration to EUR 24.32 million (funded via EUR 5 million cash and a non-cash Compulsorily Convertible Preference Share swap). This smart move preserves cash and eliminates long-term FX risks.

JCIL is moving beyond downstream processing (historically restricted to ~30% of a mill’s capex) into upstream systems like Electric Arc Furnaces (EAF) and hydrogen steelmaking. This expands its revenue opportunity per project by 2.5x to 3.3x.

The Profitability Moat: High-cost European engineering is migrating to JCIL’s Mumbai offices and Raigad workshops. This West-to-East cost migration allows for hyper-competitive global bidding and structural margin expansion.

Massive Runway: Backed by an INR 3,300 crore consolidated order book (~9x its CY25 standalone revenue), driven by massive new contract wins with JSW Steel and a planned $698 million electrical steel JV with SAIL.

Volteron™: Strategic Option vs. Direct Asset

The Reality Check: The revolutionary carbon-free electrowinning technology is co-owned at the ultimate promoter level by John Cockerill SA and ArcelorMittal—not by the listed Indian entity (JCIL).

The Upside: While it generates zero direct royalties or revenue today, JCIL serves as the global fabrication base for the group. Any future global utility-scale construction will likely route through JCIL’s workshops.

Valuation & 10-Year Trajectory

JCIL is a high-conviction growth play, trading at a steep premium (TTM P/E over 250x and P/B over 12x). The market has fully priced in flawless execution of its green steel roadmap.

The Takeaway: Near-term integration costs dragged CY25 consolidated profits into the red. However, as operating leverage from the JCMI integration takes hold, EBITDA margins are projected to scale to a stabilized 12.5%, turning JCIL into a highly profitable, globally integrated engineering giant but at Mcap of ₹ 4,495 Cr its already pricing in all the future 10 year growth rate and margin expansion.

Will they be able to do 8000 Cr in 3 years ? that’s management aspiration if you believe so you can bet on this hockey stick stock price action.

Headwinds and Enterprise Risks

Before reaching a final investment conclusion, a prudent analyst must invert the thesis and rigorously examine the primary risks capable of permanently impairing the enterprise’s earning power and, by extension, the investor’s capital.

Macroeconomic Cyclicality of the End-Market: JCIL’s revenue remains inextricably tied to the massive capital expenditure cycles of primary steel producers.10 The global steel industry is notoriously cyclical, highly sensitive to fluctuating interest rates, global GDP growth, and the influx of low-cost dumped steel (most notably from China). While the Indian government has proactively enacted measures, such as a 12% safeguard duty, to protect domestic steelmakers from foreign dumping 20, any future downturn in domestic steel profitability will result in the immediate cancellation or deferment of the capex projects that feed JCIL’s order book.

Raw Material Inflation and Execution Risk: In fixed-price EPC contracts, the contractor bears the significant risk of cost overruns. Unexpected inflation in raw materials (such as specialized steel and alloys) or delays in project execution directly and violently erode the company’s already thin operating margins. The negative profitability experienced in FY2024 is a stark historical testament to how quickly operational headwinds can result in net losses.

Governance and Capital Extraction: As analyzed previously, the parent company’s extraction of 0.6% brand fees and up to 3% technical royalties acts as a perpetual structural drag on minority shareholder returns.8 While the parent provides crucial technological know-how, this toll bridge limits the upside potential of the operating margins.

Contingent Liabilities: Legal, tax, and duty disputes are common friction points in Indian corporate operations. JCIL reportedly faces contingent liabilities of approximately ₹240.88 Crores, with some reports noting contested amounts up to ₹846.2 million related to duties and claims.29 While management may express confidence in favorable appellate resolutions and has consequently made no financial provisions 41, the sheer size of these contingencies relative to the company’s total net worth (₹210 Crores) poses a latent, non-trivial risk to the balance sheet.

The Narrative Collapse and Multiple Compression: The most acute, immediate risk to the current share price is the inevitable realization by the broader retail market that JCIL is not a direct participant in the parent company’s electrolyzer manufacturing boom. When the thematic narrative inevitably corrects and the stock is brutally re-rated back to traditional capital goods multiples (e.g., reverting to its 3-year average P/E of 76x, or the industry average of 34x), the resulting multiple compression could induce a permanent loss of capital exceeding 70% to 80% from current price levels.

Conclusion: Waiting for the Fat Pitch

The discipline of value investing requires an investor to act strictly as a rational capital allocator, evaluating businesses based on their demonstrated ability to generate durable owner earnings relative to the price demanded by the market. It requires the emotional fortitude to abstain from swinging at every pitch, resisting the FOMO (Fear Of Missing Out) generated by soaring stock charts, and waiting patiently instead for a rare opportunity where price and intrinsic value are severely dislocated in the investor’s favor.

John Cockerill India Ltd is fundamentally a respectable, viable enterprise backed by a parent company with an illustrious 200-year global engineering pedigree. The balance sheet is impeccably managed with zero debt, offering robust downside protection against bankruptcy. Furthermore, the current management team is executing a highly rational strategic pivot toward higher-margin service revenues, and the recent record standalone order backlog of ₹13 billion 10—coupled with the integration of advanced European technologies—provides strong visibility for medium-term revenue recovery.

However, a great business—and JCIL, with its single-digit returns on equity, is merely a decent business, not a great one—can instantly become a disastrous investment if purchased at an irrational price. At a multiple exceeding 150 times trailing earnings, 95 times EBITDA, and 12 times book value, the market has priced JCIL for absolute, unimpeachable perfection over the next two decades. The share price is artificially inflated by a profound market misunderstanding, conflating the parent company’s aggressive, lucrative expansion into hydrogen electrolyzer manufacturing in Kakinada with the listed Indian subsidiary’s legacy, low-margin steel EPC operations.

The current valuation leaves absolutely no margin of safety. To purchase the stock at these levels is to abandon the tenets of investment and engage in pure speculation, relying entirely on the “greater fool theory”—the hope that someone else will come along tomorrow willing to pay an even more irrational price for a stream of cash flows that cannot mathematically justify the current capitalization.

A rational, intelligent investor should admire the remarkable technological strides the John Cockerill Group is making globally in the decarbonization of the steel industry. One should applaud their joint ventures in green ammonia and hydrogen infrastructure. But one must politely, and firmly, decline the opportunity to partner with the listed Indian subsidiary at the current quoted price. The only prudent course of action is to relegate the company to the watchlist, monitor the progress of its transition toward a higher service mix, track the consolidation of its global entities, and wait for the inevitable market correction that brings the price back in line with the intrinsic value of its cash flows. In the game of investing, there are no called strikes; one must simply hold their capital and wait for the fat pitch. This, unequivocally, is not it.

📋 SEBI Statutory Disclosure & Disclaimer

Regulatory Compliance Notice: This post is for educational, informational, and research purposes only. It does not constitute a direct offer, solicitation, or recommendation to buy, sell, or hold any security or financial instrument mentioned herein.

Investors are strongly advised to consult a certified, SEBI-registered financial advisor before making any investment decisions based on this information.

How does the global acquisition change the matrix