Inventurus Knowledge Solutions Ltd

IKS Health: Curing the Economics of the $4 Trillion US Healthcare Crisis

Okay, as an investor, whenever I hear about a US healthcare opportunity, I always feel a bit like this -

Why? Because it’s a $4 trillion market growing at 6% (similar to the Indian GDP of $3.5 trillion growing at 7%), and much like India, US healthcare is one of the most inefficient markets in the world.

You might be wondering what companies in this space actually do to capture that value. Let’s look at how one company, IKS Health, is completely rewiring the economics of this system.

The “Dr. Sarah” Problem

Let’s imagine a highly skilled physician we’ll call Dr. Sarah. She spent over a decade in rigorous medical training because she wanted to save lives, solve complex medical puzzles, and connect with patients. A patient walks into her exam room, visibly anxious about a new, chronic diagnosis. In a perfect world, Dr. Sarah sits down, looks the patient in the eye, and has a deeply human, empathetic conversation.

But what actually happens today?. Dr. Sarah walks in, says hello, and immediately turns to a computer monitor. While the patient is pouring their heart out, Dr. Sarah is staring at a screen. She is furiously clicking dropdown menus, ticking compliance boxes, and wrestling with complex billing codes in an Electronic Health Record (EHR) system. She isn’t looking at her patient; she’s looking at a digital form. The system has transformed her from a healer into a highly-paid data-entry clerk.

Why is this happening? Because the hospital Dr. Sarah works for is getting crushed by a massive economic vice grip. Over the last 20 years, their operating costs have skyrocketed, but the actual Medicare reimbursements they receive have declined when adjusted for inflation. To ensure the hospital actually gets paid by the insurance companies, every single interaction must be perfectly coded and documented.

Historically, traditional tech vendors would walk into this hospital, sell them a shiny $5 million software “widget,” and say, “Good luck figuring this out!” leaving the doctors to do the heavy lifting.

Outcome Arbitrage: Flipping the Vendor Model

This is where IKS Health steps into the story, and where the business model gets fascinating from an investment perspective. IKS looks at this broken dynamic and realizes that traditional “labor arbitrage”—just selling cheap offshore human hours—is a race to the bottom.

Instead, they pioneered what we can call outcome arbitrage. IKS walks into the boardroom of a massive, billion-dollar entity like Palomar Health and changes the script entirely. They say: “We aren’t going to charge you per software license. We are going to deploy our ambient AI technology and our global workforce to completely eliminate the screen from the exam room.”.

But here is the kicker: IKS is so confident they can fix the hospital’s economics that they fronted Palomar Health $16.5 million right at the start. They tell the hospital: “If we don’t increase your operating margins by 700 to 1,000 basis points by freeing up your doctors to see more patients, you keep our cash.”. They put true skin in the game, or as seen in their deal with Western Washington Medical Group, IKS actually invested $17 million to create a Joint Venture, essentially becoming co-owners of the hospital’s business operations.

In a way, it flips IKS from being a back-office cost center to a true operational partner. Quite a transformation.

How They Actually Do It: The Scribble Suite

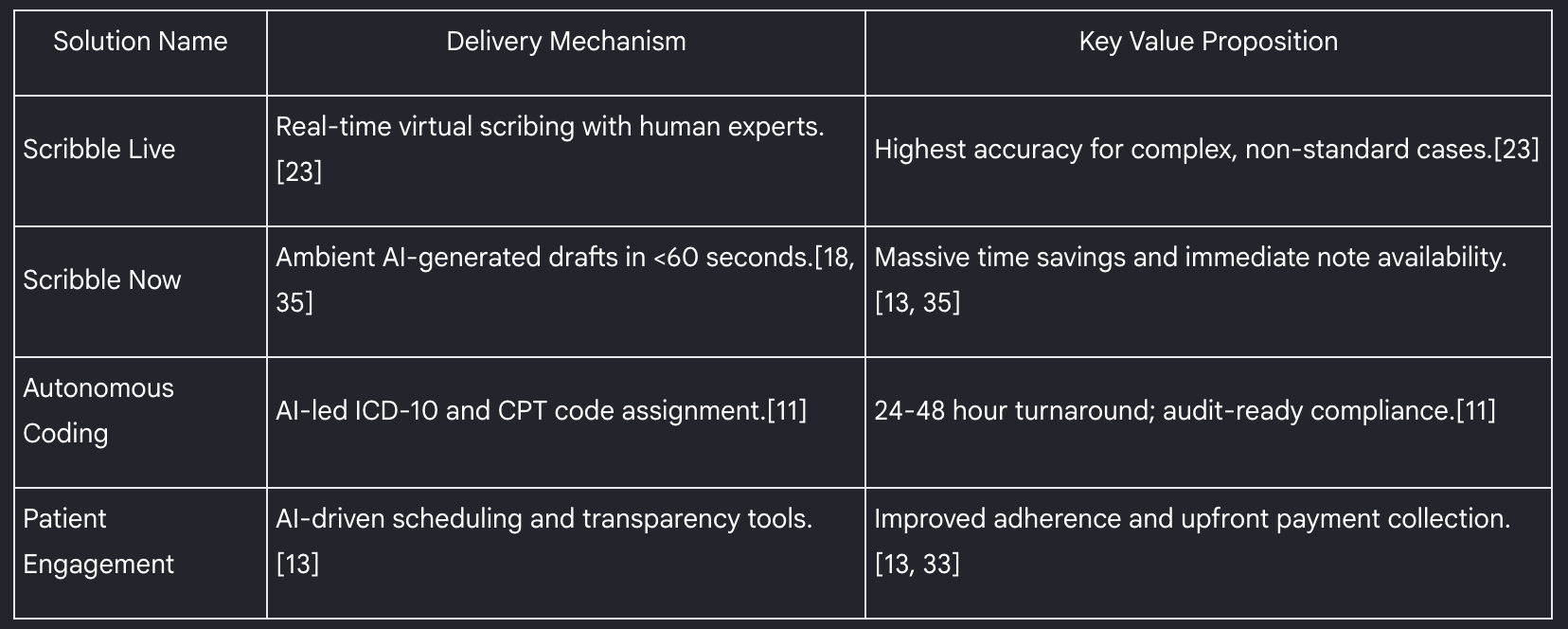

To solve Dr. Sarah’s problem, IKS Health had to fundamentally change the workflow of the exam room by removing the keyboard from the equation entirely. They deployed a proprietary system called the Scribble Suite, which is a brilliant fusion of cutting-edge technology and human infrastructure.

Here is the step-by-step breakdown:

The “Ambient” Listener: When Dr. Sarah walks into the exam room, she doesn’t log into a computer. Instead, a mobile device sits quietly on the desk. Using advanced “ambient AI” voice recognition, the system passively listens to the free-flowing conversation. Dr. Sarah can maintain 100% eye contact.

The AI First Draft: As soon as the visit ends, generative AI immediately takes the messy, unstructured audio and structures it into a highly professional, formatted clinical note. 3. The “Human-in-the-Loop” Safety Net: Raw AI can hallucinate or make medical errors. To prevent this, IKS routes that AI-generated draft to their global workforce of highly trained medical scribes and clinicians. This “Human-in-the-Loop” validates the note and applies the exact medical billing codes required.

The Invisible EHR Integration: Once validated, the perfect, error-free chart is automatically injected directly into the hospital’s massive EHR system, like Epic.

The result? For the hospital, it’s a massive win: a happier doctor who can see more patients, generating higher revenues with far fewer billing errors.

The Ultimate Economic Moat

A primary pain point for US physician groups is their tendency to seek individual point solutions for specific problems. However, IKS Health recognized that the real value lies in an integrated platform. They are possibly the only company globally offering a comprehensive platform of 16 features that cover the entire patient journey—before the visit, during the visit, post-visit, and between visits.

This creates the ultimate “sticky” business. Their top 10 customers have been with them for eight to nine years. Because their tech and human capital integrate so deeply into the client’s EMR/EHR layer, the switching costs are incredibly high. Ripping IKS out would mean crippling the hospital’s operational flow.

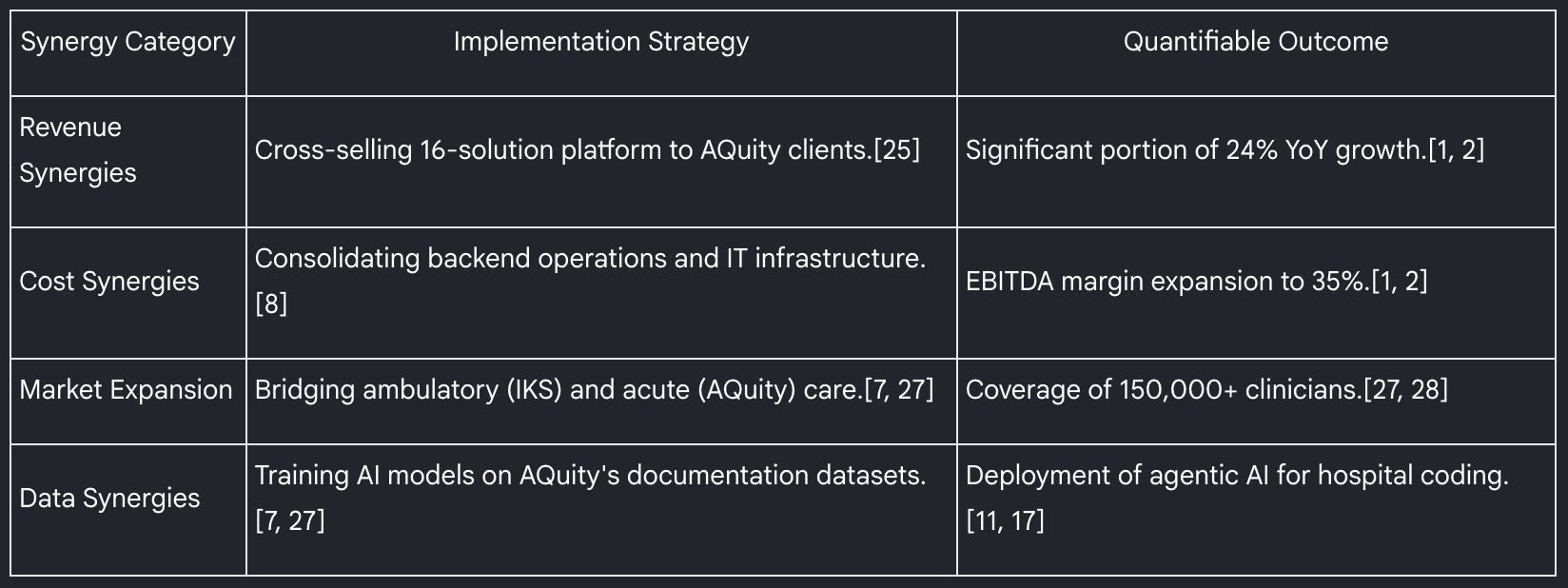

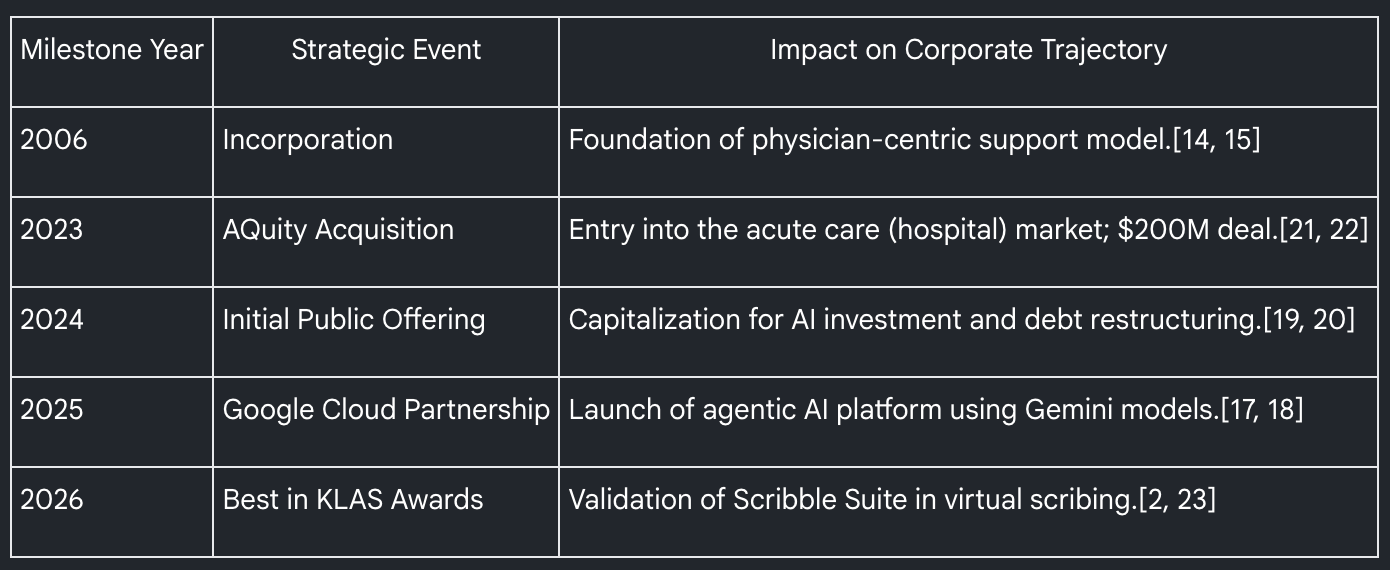

The AQuity Acquisition Catalyst

While IKS’s Total Addressable Market (TAM) in the ambulatory space is massive at around $225 billion (roughly the same size as the Indian IT services outsourcing industry), their recent acquisition of AQuity Solutions provides an explosive catalyst.

Through AQuity, IKS gained access to 800 new customers, 500 of which are massive health organizations. The combined entity now serves 155,000 physicians—nearly 18% of all physicians in America. Modeling the cross-sell impact of IKS’s 16 features across this captive base creates a mind-boggling revenue opportunity of about $28 to $29 billion.

To put that in perspective, activating just 10 to 15 of these 500 large customers could triple their entire business.

When you combine an outcome-aligned business model, a deep technological moat with high switching costs, and an 80-90x captive growth runway, you get a highly compelling investment narrative.'

Will AI disrupt them?

Good thing is founders have been evolving with technology over time -

In IKS Health’s model, the human’s role evolves through a three-phase journey:

Phase 1: Human-led with tech in the loop

Phase 2: Tech-led with human in the loop

Phase 3: Total autonomy with no human involvement, though this phase is still being approached.

Company currently transitioning from phase 2 to phase 3.

“They themselves leveraging AI to do things more efficiently”

The most profound shift in IKS Health’s technological strategy has been the transition from simple automation to “agentic” AI. Announced in late 2025, the IKS Agentic AI platform is built on Google Cloud’s Gemini family of models and its Vertex AI infrastructure. While traditional AI is designed to process data or suggest drafts, agentic AI is capable of cognitive reasoning and autonomous action within complex workflows.

For example, in the context of prior authorizations—a major administrative bottleneck in US healthcare—the agentic platform can independently detect when an authorization is required for a procedure, gather the necessary clinical evidence from the patient’s chart, and submit the request directly to the insurer’s portal. The system is estimated to autonomously handle up to 80% of routine tasks involved in insurance approvals.

The Linear to Non-Linear Pivot

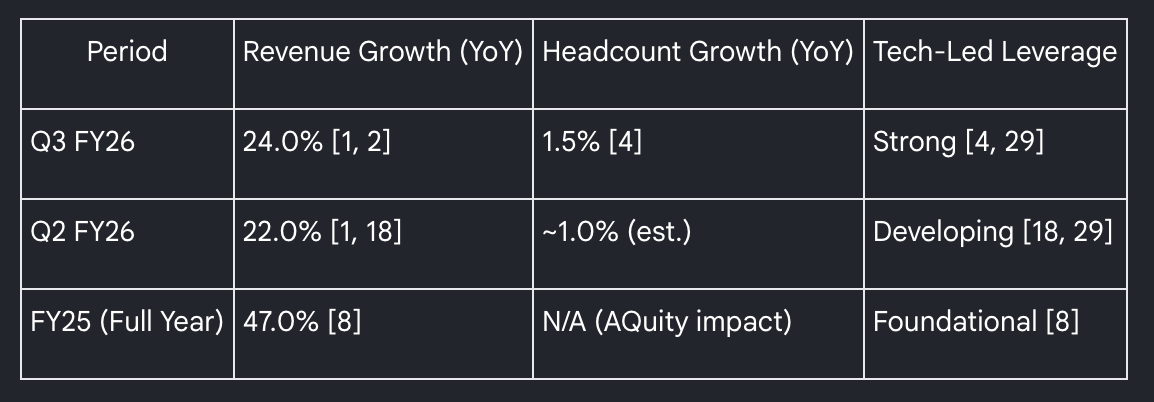

From an investment perspective, the importance of agentic AI lies in its ability to decouple revenue growth from headcount growth. Historically, IKS Health operated on a linear model common to the BPO industry. However, the Q3 FY26 results provided a definitive proof of concept for the firm’s non-linear pivot.

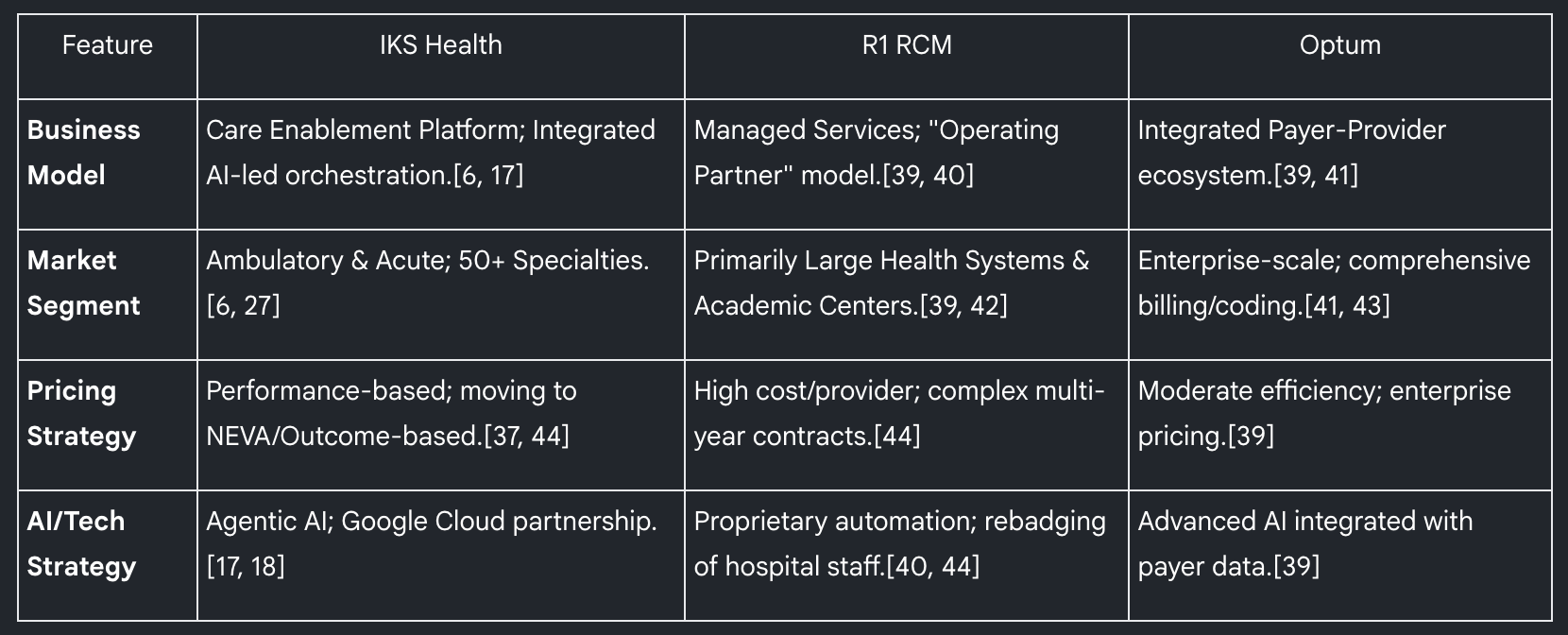

The Competitive Landscape: Why IKS Isn’t Just Another Software Vendor

If we are going to evaluate this as an investment, we have to look at the competitive moat. The US healthcare tech space is incredibly crowded. Everyone knows there is a problem, and billions of venture capital dollars have been poured into trying to fix it.

When you look at who IKS Health is up against, the market essentially splits into two distinct categories:

1. The Silicon Valley “Point Solutions” (The Pure AI Startups)

This group includes highly-valued tech startups like Abridge, Ambience, and DAX (which is owned by Microsoft). These companies build brilliant, standalone software “widgets.” For example, they might build a fantastic AI ambient scribe that listens to the doctor and writes a note.

Their Weakness: They are just selling software. They drop the tool into the hospital’s lap and say, “Here is a great AI transcriber.” But the hospital still has to figure out how to integrate it into their Electronic Health Record (EHR) system, train their staff to use it, and build workflows around it. It’s fragmented.

The IKS Advantage: IKS’s CEO, Sachin Gupta, actively bets against this model. IKS doesn’t sell a “point solution”; they sell a comprehensive 16-feature platform. They don’t just transcribe the note; their “Human-in-the-Loop” team validates the AI, assigns the billing codes, and pushes it directly into the hospital’s backend. They take over the entire workflow.

2. The Legacy RCM Behemoths (The Big Outsourcers)

On the other end of the spectrum are the massive, traditional Revenue Cycle Management (RCM) giants like R1 RCM, Optum, and Oracle Health. These are the enterprise heavyweights that typically focus on large academic medical centers and massive hospital networks.

Their Weakness: Many of these legacy players still rely heavily on traditional labor arbitrage (throwing cheap offshore bodies at a billing problem) or charge high, complex per-provider fees. Their models can be rigid, and they often focus strictly on the backend (collecting the money) rather than fixing the clinical experience in the exam room.

The IKS Advantage: IKS competes here by completely changing the pricing dynamic. While a giant like R1 RCM might charge expensive monthly fees and lock hospitals into rigid contracts, IKS utilizes its “Net Economic Value Add” (NEVA) model. IKS is willing to put capital upfront (like the $16.5M guarantee with Palomar) and tie their revenue strictly to the margin improvement they deliver. Furthermore, IKS operates across the entire care continuum—not just billing, but actually freeing up the doctor’s time.

One of the most significant developments in 2025-2026 has been the launch of "Scribble Now," an ambient AI scribing solution. Unlike virtual scribing, which involves a live human, ambient AI utilizes microphones in the exam room or telehealth platform to listen to the patient-clinician conversation and automatically draft a structured clinical note.[17, Clinical studies have shown that this technology can reduce documentation time by 2-3 hours daily, allowing physicians to see up to 15% more patients per hour while significantly reducing burnout.

Competitive Landscape and Peer Benchmarking

IKS Health operates in a highly competitive market populated by global healthcare giants (but IKS health is winning marketshare from last 5 years given their growth rate), specialized RCM firms, and emerging AI pure-players. The company’s primary competitors include R1 RCM, Optum (a subsidiary of UnitedHealth Group), and AGS Health.

Direct Competitor Comparison

The market for Revenue Cycle Management and clinical documentation is currently undergoing consolidation. Firms are being evaluated based on their ability to integrate AI into existing EHR (Electronic Health Record) workflows.

A key differentiator for IKS Health is its "Scribble" suite's integration into the revenue cycle. While competitors like R1 RCM focus heavily on the backend financial operations, IKS begins its value creation at the point of care with documentation, ensuring that the financial data is "clean" from the moment it is generated.

Ambient AI Scribing: A Crowded Sub-Market

In the specialized field of ambient AI documentation, IKS Health competes with heavyweights such as Microsoft-owned Nuance (DAX), Abridge, and Suki AI. As of late 2025, Microsoft/Nuance and Abridge control nearly two-thirds of the $600 million ambient AI scribe market. However, IKS Health’s strategy is not to win as a standalone “point solution” scribe but as an integrated platform.

Market data from Menlo Ventures suggests that while Abridge has built strong momentum in primary care and templated specialties, IKS Health’s “Scribble Live” remains a preferred choice for complex, specialty-specific documentation where 100% accuracy is non-negotiable. The 2026 Best in KLAS award for IKS Health’s virtual scribing services highlights the company’s ability to maintain high satisfaction scores (91.9 out of 100) even as the industry pivots toward pure AI.

The Investment Takeaway: The “Platform” Moat

The reason IKS is winning deals against both nimble AI startups and multi-billion-dollar RCM giants comes down to integration.

Hospitals are exhausted by “vendor fatigue.” They don’t want to buy a transcription tool from Microsoft, a billing service from Optum, and a patient scheduling tool from someone else. They want a single, structural partner who will take on the operational risk. By combining Google Cloud-backed Agentic AI with a global workforce of clinically trained experts, IKS embeds itself so deeply into the hospital’s nervous system that ripping them out becomes nearly impossible.

That high switching cost, combined with a willingness to co-own the financial outcomes, is what builds a durable economic moat.

Where is the Future Growth Coming From? The Strategy Unpacked

When you analyze a company that has already scaled rapidly, the immediate question for any investor is: What’s the next catalyst? How do they keep growing revenue, and how much of that actually flows down to the bottom line?

For IKS Health, the roadmap for the next three to five years is built on two very specific pillars: breaking the linearity of human labor, and aggressively mining their own backyard.

Revenue Growth: The 80/20 “Land and Expand” Rule

If you look at the management’s commentary from their recent Q3 FY26 earnings, they revealed a fascinating statistic. They expect 85% to 90% of their future incremental growth to come from existing customers, rather than hunting for brand-new logos.

Remember that AQuity acquisition we talked about? IKS bought access to 500 massive health systems that were previously just buying single “point solutions” (like basic transcription). IKS has now stratified the top 50 of those legacy accounts. Their entire go-to-market engine is geared toward walking into those 50 hospitals and saying, “You already trust us with your clinical notes. Let us take over your entire revenue cycle and coding processes too.”

But here is the most important metric that proves their business model is evolving: Breaking Linearity. Historically, in the BPO or healthcare services space, if you wanted to grow revenue by 20%, you had to hire 20% more people. It was a linear, labor-heavy trap. In Q3 FY26, IKS Health reported a massive 24% year-over-year revenue jump. But their employee headcount only grew by 1.5%. That spread is the holy grail for a services business. They are successfully using their new “Agentic AI” platform—built in partnership with Google Cloud—to automate the heavy lifting of medical coding and billing. The AI handles the volume, while the human experts handle the edge cases.

The Margin Reality: Reinvesting the AI Surplus

So, if AI is making them so efficient, will their profit margins just keep climbing to the moon?

Actually, no. And this is a sign of disciplined management.

Right after the AQuity acquisition, their blended EBITDA margins dipped into the mid-20s. Over the last few quarters, they have aggressively optimized that business, bringing their current EBITDA margins up to a very healthy ~35%.

But management—led by CEO Sachin Gupta and CFO Nithya Balasubramanian—has explicitly stated that they are not trying to push structural margins much higher than this “early-to-mid 30s” range.

Instead of hoarding the operational savings generated by their AI platforms, they are going to reinvest that surplus directly back into the business. They are funneling that cash into R&D (which currently sits at nearly 5% of their revenue), platform expansion, and a stronger sales force.

As an investor, this tells you exactly how to model their future. Their future earnings growth isn’t going to come from squeezing extra pennies out of their profit margins. It is going to be almost entirely revenue-led. They are choosing to maintain healthy, stable margins in the 30s so they can continuously fund the technology needed to capture a larger slice of a $34 billion outsourced addressable market.

It is a classic “delay short-term optimization for long-term market dominance” strategy. For a business sitting on a 99% client retention rate with massive cross-sell opportunities, it’s exactly the playbook you want to see.

Financial Analysis and Quarterly Performance Deep Dive

The financial trajectory of Inventurus Knowledge Solutions Limited reflects its successful transition from a private, service-oriented firm to a public, technology-enabled platform. The consolidated figures for the third quarter of fiscal year 2026 demonstrate consistent growth and robust operational efficiency.