Computer Age Management Services Ltd (CAMS)

CAMS, business model, #valuation, intrinsic value, #stock, #share

In this blog post, I’ll try to value another wonderful business as we have done for Nykaa, SBI Cards, and MapMyIndia in the last three posts.

The reason is there is no denying the fact that these are the greatest of the great businesses but because everyone knows these are great businesses they have always traded at a crazy valuation which only made sense to folks like Marcellus, As markets are voting machine over the short term and weighing machine over a long run thankfully there is some correction happening in these stocks lately and we should at least have some idea about their intrinsic value in order to buy them if at all they fall into the value category.

Let’s start with understanding about CAMS business model.

What Is CAMS And What Does It Do?

This is an organization used by Mutual Fund companies and other financial institutions to record transactions and maintain these records. Essentially, transfer agents in the Mutual Fund industry will help maintain records of buying and selling of securities within funds, also calculate and disburse dividends and help prepare and mail shareholder account statements.

CAMS offers Distributor Services packages to all distributors who operate using retail sub-agents.

The services include –

Maintenance of sub-brokers details

Maintenance of investor details

Import of investors’ daily transaction details

Import of month-end net asset positions

Import of month-end trailer fees payable

Computation of incentives payable to sub-brokers for sales

Computation of commission payable to financial consultants for sales

Front-end commissions payable to sub-brokers

Trailer fees payable to sub-brokers

Target-based incentive commissions payable to sub-brokers

System to view investors’ portfolios under one client number

CAMS also provides technology-based service solutions to Life Insurance companies, Private Equity Funds, banks, and Non-Banking Finance Companies (NBFC). CAMS is also an approved GST Suvidha Provider (GSP).

Basically, CAMS acts as a custodian of customers’ data, it takes special care to maintain complete confidentiality of the data.

CAMS serves 10 of Top 15 AMCs with nearly 3x AuM of the 5 MFs serviced by other RTA.

And they have been gaining market share due to a superior customer base and winning new marque clients.

After understanding the businesses - one question could come to your mind why AMCs doesn’t do it themselves? why are they outsourcing it?

Frankly, I wondered about it too and found out that apart from Franklin AMC everybody is outsourcing it and in 2020 even Franklin folded & decided to outsource it.

So, this is safe to assume that these guys will remain in business as long as AMCs are in business. Moreover of the Rs 26 lac Cr of AUM they are managing they make only Rs 900 Cr of revenue meaning this expense to the MF AMC companies is small enough that they would care about optimizing (As it’s so small compared to other expenses they have).

When asked what differentiates them From the competition -

Anuj Kumar: Sure. Good question. And, you know, as you gain intimacy with the business, Dushyant, over a period, you will kind of realize this better. But if I were to sum it up, it is not the license, which serves as the differentiator. There are two, three parts to this entire construct. One is like, it is a very nuanced, multilayered, detailed, complex understanding of process and regulation both. Now, that sounds like a line of English. But when you start practicing it, it is what it is. And I come from a background of outsourcing and multiple industries. And I have seen including England, India, and overseas, including healthcare, airlines, telecom, all of that. And this is extremely nuanced and multilayered. And therefore, the base of knowledge and the base of processing that we built over the last many years, and this entire workforce is a large asset, and our ability to kind of understand regulation and then build a process and execution around that. And the second, the biggest part of this is the platform, because the platform is what the business gets done on. And like you know, all the components of the platform, whether it is for processing or data keeping, long-term record keeping, brokerage computation, all of those things are being done on our central platform. That is the IP -- it has taken us about two-and-a-half decades to bring that entire platform to the current level. There are no commercial sellers in India of that kind of platform. There are commercial sellers overseas but porting that platform to the needs of the Indian market is extremely tough, cumbersome, and cruddy. And some people have tried that, and it has not been successful. So, the successful RTAs that you see today have both ridden on bespoke own platforms over the last the last two, three decades.

And then the third, of course, is that we have created this vast financial infrastructure, both physical and electronic. The physical infrastructure is the network of 270, branches, the 1500 people who work there, service, investors, and distributors, and the electronic infrastructure is all the linkages that we've created with all the other constituents, like the AMCs, the 100,000 registered distributors, payment aggregators, stock exchanges, all of those. So, if you put these three components, that is really what I would classify as the, the build, the IP part of the business, which is tough to replicate. I would not think of the license as the key component of the secret sauce.

What are the revenue growth drivers?

CAMs revenue grows with the growth in AMCs AUM, CAMs get the % cut of the AUM they are managing for the AMC but due to pricing being a tiered structure, when the AAuM grows, their asset-based fee, which constitutes almost the bulk of the revenue would grow with a lag to the asset growth.

What is a tiered pricing structure?

Tiered pricing as a model (also known as price tiering) is used to sell your products within a particular price range. Once you fill up a tier you move to the next tier and you will be billed according to the number of purchases you make in those respective tiers.

For example, one way you could price is -

suppose you’ve sold 60 widgets to your customer. In a tiered pricing model, you calculate your total like this: [($20x10) + ($10x20) + ($5 x 30)] = $550.

You move to the next tier only when one tier is completely filled.

Whereas in Volume pricing you will just do $5 * 60 = $300.

Many companies in the SaaS space most commonly have three tiers to differentiate the price points and some, even more. The main idea behind a tiered pricing strategy is that your prices and features should be tailored according to the various needs and use cases of the customers you’re selling to.

You will have to be careful about deciding the value metric and the cost for the respective tiers.

So, it’s important to understand in deep about the CAMs tiered pricing model to have a fair idea that indeed they are a proxy to AMC industry growth overall.

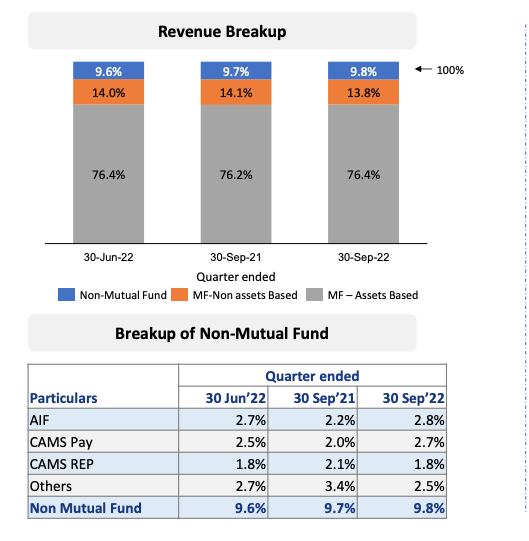

So far we have learned that a Major part of the revenue earned by MF RTAs (CAMS) (approximately 80%) is by means of fees charged on the AUMs managed by the AMCs for which CAMS provides the services.

The sad thing is these fees are generally tiered in nature and tend to decrease as a proportion of the total AUMs of the fund house once the AUMs surpass the tiers for which the fees are agreed on.

Also, the other major portion of revenue is the charge for handling paper-based transactions of AMCs, for which considerable effort is needed to enter the details into the system for effective record keeping and reporting, for which AMCs pay the high processing fee vs the digital and now due to digitization, this portion of revenue is going down as well.

and MF RTAs charge the highest fee for equity AUMs then Debt AUM then liquid and last is Index and ETFs.

Just to give you some perspective, HDFC AMC makes about a 0.5% fee (revenue) on the total AUM they manage. If you take the weighted average of the above table these guys are charging roughly 0.04% of the AUM which is about 8% of the revenue AMCs are making.

Just to give you a global perspective Vanguard makes 0.1% fee (revenue) as a % of AUM, So if HDFC AMCs fee continues to slide down to 10 or 20 basis points then we should expect similar pressure RTA fee as well.

Shown below- how currently the pie is getting divided on the fee you and i pay to the MF.

Another pressure on the revenue growth of RTA (CAMS) will come from the tiered pricing model anyways as the AUM of the industry continues to grow. To prove this point since 2011 the AUM of the AMC industry grew at 13% cagr and CAMs despite growing market share from 56% to 70% grew at 12-13% cagr. Now if you think the market share growth has plateaued then it’s hard to say they will continue to grow revenue at a similar rate of AUM growth in the MF industry. I think realistically we should not expect CAMs to grow more than 12-13% in the next decade & all the margin growth has already happened maybe with some operating leverage they may be able to grow net profits at 15% cagr (best case scenario i my view, not sure why folks paid 80PE for this stocks at its peak).

Another thing we have to consider while valuing it They charge the highest fee for managing Equity AUM and Lowest for managing Index and ETF funds, Today I think there should not be any doubt that ETFs AUM going to grow at a rate higher than the industry. This means the 0.03-0.04% of the AUM fee they are making may decline as the ETF portion of the AUM grows over time.

Other sources of revenue?

Other sources of revenue constitute 24% of total revenue, which I think will grow in line with their main revenue.

The reason stock has been correcting is markets are finally trying to price in the cyclicality of the business (mid-single digital growth cycle) but I think markets haven’t really priced in yet the 12-13% revenue growth or maybe 15% pat growth for the company over the long run. As shown below Q2 FY23 has low single-digit growth everywhere.

Now as the earnings are reverting to mean the stock has corrected to 40 times earnings. So, is it trading now cheap enough? Let’s see what the growth markets are pricing into the stock today.

Markets are pricing in the 20% growth rate for the next 15 years, which actually didn’t happen even in the past when it grew from a low base with margin expansion.

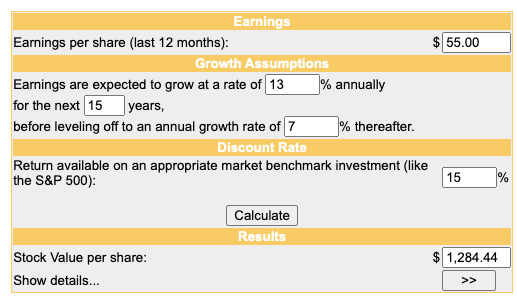

If we work with more realistic growth expectations like 13-15% cagr growth for the next 15 years and 7% terminal growth we get around Rs 1200-1560 stock value per share.

which is about 30 to 40% lower than what it’s trading at today. Let’s wait and watch hopefully Mr market may provide an opportunity to buy it at a reasonable price one day.

Good analysis.

Your view on icici sec and angel one?

Seems the valuation is right on these two. If a bull market comes, shouldn't these 2 will beat cams on return?